Fill Out My Promissory Note

Fill Out My Promissory Note

Fillable Promissory Note Document

A Promissory Note is a financial document where one party promises in writing to pay a specific sum of money to another. This form outlines the details of the repayment, including the payment schedule, interest rate, and what happens if the borrower fails to repay. It serves as a legal proof of debt between the borrower and the lender.

Overview

In an era where financial transactions have become vastly complex, the need for straightforward, enforceable agreements is more pronounced than ever. Central to these agreements, particularly in the realm of lending and borrowing, is the Promissory Note. This significant document serves not only as a binding promise by a borrower to repay a sum of money under specific terms but also outlines the repercussions of failing to fulfill this commitment. Covering interest rates, repayment schedules, and the roles of both the lender and the borrower, a Promissory Note form ensures clarity and security for all parties involved. Moreover, it stands as an essential tool in the prevention of disputes, providing a legal framework that can be referenced by courts in case of a disagreement. The utility and importance of this document cannot be overstated, acting as a linchpin in personal loans, business financing, and a myriad of other financial agreements that fuel the economy.

- Alabama

- Alaska

- Arizona

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- District of Columbia

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming

Promissory Note Types

Sample - Promissory Note Form

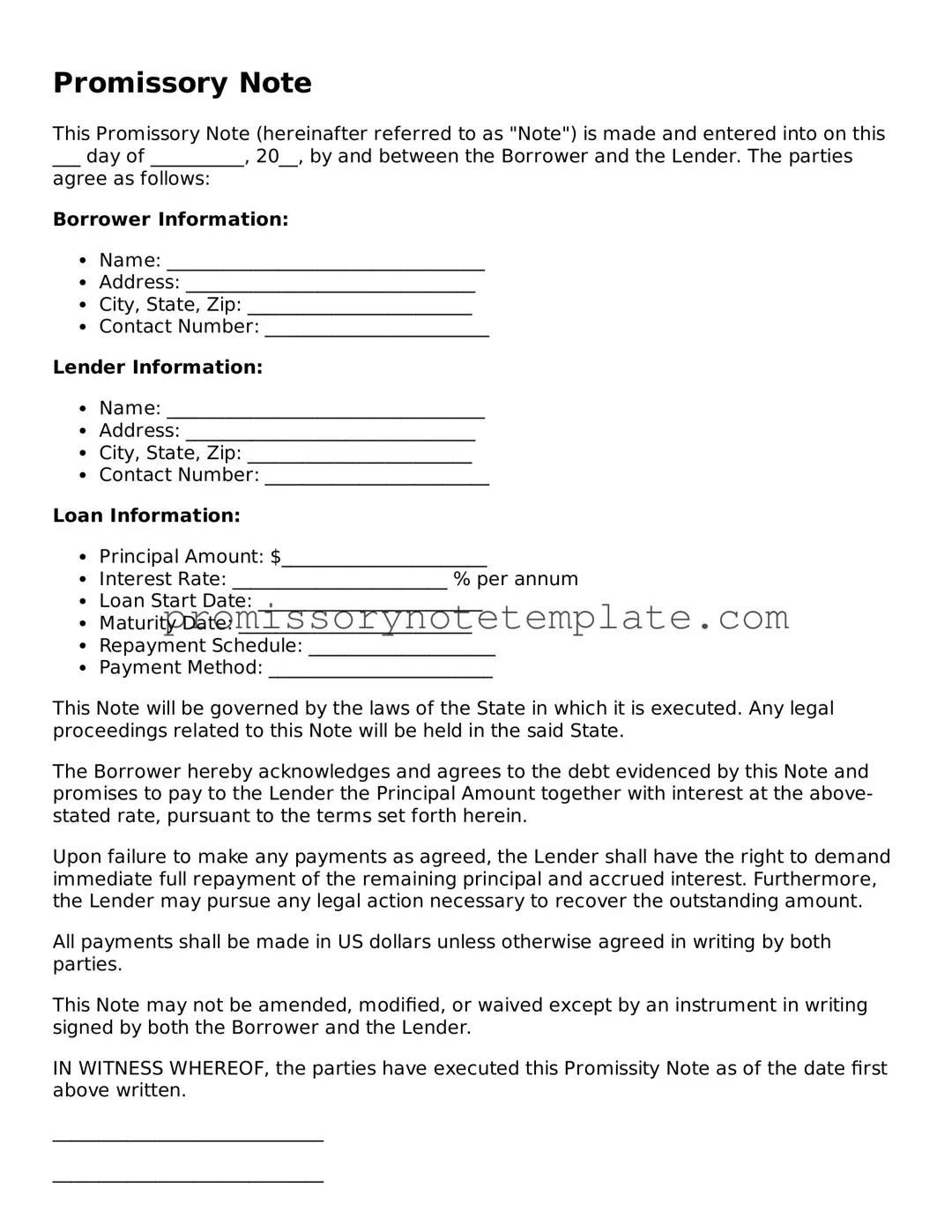

Promissory Note

This Promissory Note (hereinafter referred to as "Note") is made and entered into on this ___ day of __________, 20__, by and between the Borrower and the Lender. The parties agree as follows:

Borrower Information:

- Name: __________________________________

- Address: _______________________________

- City, State, Zip: ________________________

- Contact Number: ________________________

Lender Information:

- Name: __________________________________

- Address: _______________________________

- City, State, Zip: ________________________

- Contact Number: ________________________

Loan Information:

- Principal Amount: $______________________

- Interest Rate: _______________________ % per annum

- Loan Start Date: ________________________

- Maturity Date: _________________________

- Repayment Schedule: ____________________

- Payment Method: ________________________

This Note will be governed by the laws of the State in which it is executed. Any legal proceedings related to this Note will be held in the said State.

The Borrower hereby acknowledges and agrees to the debt evidenced by this Note and promises to pay to the Lender the Principal Amount together with interest at the above-stated rate, pursuant to the terms set forth herein.

Upon failure to make any payments as agreed, the Lender shall have the right to demand immediate full repayment of the remaining principal and accrued interest. Furthermore, the Lender may pursue any legal action necessary to recover the outstanding amount.

All payments shall be made in US dollars unless otherwise agreed in writing by both parties.

This Note may not be amended, modified, or waived except by an instrument in writing signed by both the Borrower and the Lender.

IN WITNESS WHEREOF, the parties have executed this Promissity Note as of the date first above written.

_____________________________

_____________________________

State-Specific Acknowledgment (if applicable):

This Note shall be subject to the specific provisions and regulations of the state of _______________, as applicable.

PDF Form Features

| Fact Name | Description |

|---|---|

| Definition of Promissory Note | A promissory note is a financial document in which one party promises to pay another party a specified sum of money at a specified time or on demand. |

| Components | Key components typically include the amount borrowed, interest rate, repayment schedule, and the signatures of the involved parties. |

| Usage | It is widely used in personal loans, business loans, and real estate transactions to create a legal obligation to repay borrowed funds. |

| Governing Laws | Governing laws may vary by state, but all promissory notes are subject to the uniform commercial code (UCC) in the United States to some extent. |

How to Use Promissory Note

Filling out a Promissory Note is a crucial step in documenting a loan between two parties. It serves as a binding legal agreement that outlines the borrower's promise to repay the sum lent, under specified conditions. This formalization aids in preventing misunderstands and ensures clarity regarding the loan terms. The process of completing the promissory note should be approached with attention to detail, to accurately reflect the agreement between the lender and the borrower.

- Gather all necessary information, including the full legal names of the lender and the borrower, the loan amount, interest rate, and repayment schedule.

- Start by entering the date on which the promissory note is being created at the top of the document.

- Write the full legal names of the borrower and the lender, ensuring correct spelling and any titles or suffixes.

- Specify the principal amount of the loan in words and then in numbers to prevent any ambiguity.

- Clearly state the interest rate, expressed as an annual percentage, that will apply to the loan.

- Determine the repayment schedule and include detailed information such as the number of payments, the amount of each payment, and the due dates for these payments. Specify whether the loan is to be repaid in installments or a lump sum.

- If applicable, describe any collateral that the borrower is using to secure the loan. Include a clear description of the collateral and any registration identifiers if relevant.

- Discuss and decide on provisions for late payments or default. Specify any late fees or actions that will be taken if the borrower fails to make payments according to the agreed schedule.

- Both the borrower and the lender should sign the promissory note. Include a space for signatures, printed names, and the date of signing at the bottom of the document.

- Consider having the signatures notarized to add an extra layer of legal validation, though this step is not always required.

After the promissory note is fully completed and signed, both parties should keep a copy for their records. This document will serve as a legal record of the loan terms and the commitment to fulfill them. It's advisable for the lender to hold the original document until the loan is fully repaid. Following these steps carefully will help ensure that the loan process is transparent and that both parties are protected.

Frequently Asked Questions

What is a Promissory Note?

A Promissory Note is a legal document that outlines a promise by one party, the borrower, to repay a specified sum of money to another, the lender, under agreed-upon terms. This document contains the details of the loan, such as the amount borrowed, interest rate, repayment schedule, and the consequences of non-payment.

Who needs a Promissory Note?

Any individual or entity that intends to lend or borrow money with the expectation of repayment should use a Promissory Note. It provides a legal framework that protects both parties’ interests, clarifying the terms of the loan and ensuring there is a written record of the agreement.

Is a Promissory Note legally binding?

Yes, a Promissory Note is a legally binding document. Once both parties have signed the agreement, they are legally obligated to follow the terms outlined within the document. Failure to do so may allow the injured party to pursue legal action to enforce the agreement or seek damages.

What are the essential elements of a Promissory Note?

A Promissory Note must include the amount of money being borrowed, the interest rate if applicable, repayment terms (including amounts and due dates), both parties’ legal names, and signatures. It may also specify collateral securing the loan and the consequences of defaulting on the loan.

How does one enforce a Promissory Note?

Enforcement of a Promissory Note typically involves legal proceedings where the lender seeks a judgment against the borrower for the amount owed. This process can vary significantly depending on local laws. If the loan is secured by collateral, the lender might also have the right to seize the collateral as a form of repayment.

Can a Promissory Note be modified?

Yes, a Promissory Note can be modified, but any changes to the agreement must be approved and signed by both the borrower and the lender. The modifications should be documented in writing to maintain the legal integrity of the note.

What happens if a borrower defaults on a Promissory Note?

In the event of a default, the lender may take legal action to recover the outstanding balance. The specific recourse available, such as collateral seizure or wage garnishment, depends on the terms of the Promissory Note and applicable state laws. Typically, the lender will first issue a notice of default to the borrower, offering an opportunity to cure the default before taking further action.

Are there different types of Promissory Notes?

Yes, there are several types of Promissory Notes, including secured and unsecured notes, demand notes, and installment notes. The type used depends on the agreement between the borrower and lender, such as whether collateral is being used to secure the loan or how repayment is structured.

Does a Promissory Note need to be notarized or witnessed?

The requirement for notarization or witnesses varies by state. While not always mandatory, having the document notarized or witnessed can add a level of authenticity and may help in the enforcement of the note.

Can a Promissory Note be transferred to someone else?

Yes, a Promissory Note can be transferred to another party unless it explicitly states otherwise. This process is known as assignment. The new holder of the note gains the right to collect the debt under the same terms as the original lender. It is crucial that the transfer of the note is documented to ensure the legal rights are properly transferred to the new holder.

Common mistakes

Filling out a promissory note might seem straightforward, but it's easy to make mistakes that could have significant financial and legal consequences. A promissory note is a binding agreement between a borrower and a lender, where the borrower promises to pay back a specified sum of money by a set date. Due to its legally binding nature, it's crucial to complete this document carefully. Here are five common mistakes people make when filling out a promissory note form:

-

Not specifying the exact terms of the loan. One of the most critical components of a promissory note is the detailed terms of the loan. These terms include the loan amount, interest rate, repayment schedule, and the final due date. Omitting any of these details can lead to confusion and disputes down the line. It's essential to specify these terms clearly to ensure both parties have a mutual understanding of the agreement.

-

Failing to include the interest rate or incorrectly calculating it. The interest rate of a loan is a vital element that must be accurately stated in the promissory note. Neglecting to include the interest rate or miscalculating it can lead to significant financial discrepancies. This oversight not only affects the total amount to be repaid but can also lead to legal issues if the interest rate applied exceeds the maximum allowed by law.

-

Overlooking the need for a co-signer. Sometimes, especially in cases where the borrower's creditworthiness is in doubt, a co-signer is necessary to secure the loan. A co-signer is someone who agrees to pay back the loan if the primary borrower fails to do so. Failing to determine if a co-signer is needed and, if so, not having them sign the promissory note, is a mistake that can expose the lender to unnecessary risk.

-

Forgetting to include a clause about late fees or penalties for default. A comprehensive promissory note should also outline the consequences for late payments or defaulting on the loan. This includes any late fees or penalties and the conditions under which the lender can demand full repayment. Such clauses protect the lender's interests and encourage timely repayment. Without these provisions, enforcing penalties or taking legal action in the event of non-payment becomes more challenging.

-

Not signing or dating the document. It sounds basic, but it's surprisingly common for one or both parties to forget to sign or date the promissory note. A promissory note is not legally binding until it has been signed by both the borrower and the lender. Moreover, the date of agreement is crucial for establishing the timeline for repayment and any legal proceedings that may follow. This final step, while simple, is essential for the note's validity.

Avoiding these mistakes requires attention to detail and an understanding of the legal implications of each part of a promissory note. It is often advisable to seek legal guidance when drafting or signing any legally binding document to ensure all parties are protected and the terms are clear and enforceable. By being meticulous and informed, individuals can navigate the complexities of promissory notes more effectively, fostering trust and security in their financial transactions.

Documents used along the form

When dealing with a Promissory Note form, it's crucial to understand that it is just one of several documents that might be needed in financial transactions or loans. A Promissory Note is essentially a written promise to pay a specific amount of money to a specific person within a set timeframe. However, to ensure the terms are clear, enforceable, and protected, other documents are often used alongside it. Here is a list of some of those documents that are frequently needed to support or clarify the terms and conditions of a Promissory Note.

- Loan Agreement: This outlines the terms of the loan in detail, including the responsibilities of both the lender and the borrower. It is more comprehensive than a Promissory Note and can offer more protection to both parties.

- Security Agreement: If the loan is secured with collateral, this document details the collateral securing the loan, ensuring the lender can claim it if the loan is not repaid.

- Guaranty: This is an agreement where a third party promises to repay the loan if the original borrower fails to do so, providing an additional layer of security for the lender.

- Mortgage or Deed of Trust: For real estate transactions, this secures the loan with the property being purchased, allowing the lender to foreclose on the property if the borrower defaults on the loan.

- Amortization Schedule: This document provides a breakdown of each payment over the life of the loan, detailing how much goes toward the interest and how much towards the principal balance.

- UCC-1 Financing Statement: If the loan involves personal property as collateral, this form is filed to publicly declare the lender's interest in the collateral.

- Disclosure Statement: Required for most consumer loans, this outlines the terms of the loan, the interest rate, fees, and other charges in a clear, easy-to-understand way.

- Co-signer Agreement: If someone is co-signing the Promissory Note, this agreement outlines the co-signer's obligations, making them legally obligated to repay the loan if the primary borrower does not.

- Acceleration Clause: While this may be a part of the loan agreement, it's crucial enough to mention separately. It stipulates that the entire balance of the loan can become due immediately if the borrower fails to meet certain conditions.

Each of these documents plays a vital role in the lending process, offering clarity and legal protection to all parties involved. Whether you're the lender or the borrower, being prepared with the right documentation can streamline the process, prevent misunderstandings, and safeguard your interests. Remember, dealing with loans and financial transactions can be complex, and it's always wise to consult with a professional to ensure that all your bases are covered.

Similar forms

The Promissory Note form is similar to a Loan Agreement, but with a simpler layout and usually for a more personal context. A Loan Agreement is comprehensive, detailing the terms and conditions of a loan between two parties, including interest rates, repayment schedules, and legal actions in case of default. By contrast, a Promissory Note keeps things straightforward – focusing mainly on the repayment amount, interest rate if applicable, and the due date. It serves as a binding promise from the borrower to the lender to pay back a specified sum of money within a set timeframe, without delving into the extensive legalities that a Loan Agreement entails.

Another document closely related to the Promissory Note is the IOU (I Owe You). Both establish an obligation to repay a debt, but the degree of formality and detail distinguishes them. An IOU is an informal acknowledgment of a debt, usually devoid of specifics like repayment dates and interest rates. It simply records that one party owes another a certain amount of money, making it less binding than a Promissory Note, which outlines the repayment terms more thoroughly. While an IOU might suffice for small, trust-based transactions between individuals who know each other well, a Promissory Note is preferred for its legal enforceability and specificity.

Mortgages and Promissory Notes also share some similarities, particularly in their function of documenting a loan that needs to be repaid. However, a mortgage is specifically tied to real property as collateral for the loan. The borrower agrees that if they fail to make payments, the lender can take possession of the property to recover the owed amount. This collateral aspect is what sets mortgages apart. Promissory Notes can involve loans for various purposes, not necessarily secured by property. They emphasize the promise to repay, regardless of the loan's use, making them more versatile but potentially less secure for the lender.

Dos and Don'ts

When filling out a Promissory Note form, individuals are dealing with a legal document that outlines their promise to pay back a sum of money. The clarity, accuracy, and thoroughness of this document are paramount. To ensure these elements are met, there are specific practices one should follow and others that should be avoided. Below are essential dos and don’ts when completing a Promissory Note form.

Do:

- Ensure that all parties involved (borrower and lender) are clearly identified with full legal names to avoid any ambiguity.

- Completely fill out the form without leaving any blank fields to prevent misunderstandings or potential tampering after the document has been signed.

- Include specific details about the loan, such as the principal amount, interest rate, repayment schedule, and late fees, if applicable, for full transparency.

- Sign and date the document in the presence of a notary or witnesses (as required by your jurisdiction) to add a layer of legality and authenticity.

Don’t:

- Use vague language or terms that could be subject to interpretation. Be clear and precise in your wording to ensure the agreement's terms are understood by all parties.

- Forget to specify the conditions under which the note can be amended or what happens in the event of a default. These details provide a clear roadmap should complications arise.

- Ignore state laws regarding lending and borrowing, which can include specific requirements about maximum interest rates and necessary disclosures.

- Rely solely on generic templates without ensuring that all sections are relevant to your specific agreement and compliant with local laws.

Misconceptions

Many people harbor misconceptions about Promissory Notes, leading to confusion and errors in their use and interpretation. By clarifying these misconceptions, individuals can better understand the legal and financial implications of these documents.

All Promissory Notes are essentially the same: This is incorrect. Although they share a basic structure, Promissory Notes may vary markedly depending on the nature of the loan, state laws, and specific terms agreed upon by the parties involved. It's important to customize each Note to fit the specific agreement.

Promissory Notes are only for financial institutions: Not true. While banks and other financial institutions frequently use Promissory Notes, individuals can also use them for personal loans between family members or friends. They serve as a formal agreement to ensure repayment under agreed-upon terms.

A verbal agreement is as binding as a written Promissory Note: This is a dangerous assumption. While verbal contracts can be enforceable, a written Promissory Note provides clear evidence of the agreement and its terms, which is crucial in the event of a dispute.

Once signed, Promissory Notes cannot be modified: This is incorrect. The parties involved can modify a Promissory Note, but any changes should be documented in writing and signed by all parties, much like the original agreement.

A Promissory Note is the same as an I.O.U.: Though both acknowledge a debt, a Promissory Note includes more detailed information, such as the payment schedule, interest rate, and the consequences of non-payment. An I.O.U. is more informal and typically includes less detail.

Promissory Notes do not require witnesses or notarization: The need for witnesses or notarization depends on the state laws and the amount of the loan. While not always required, having the Note witnessed or notarized can add a level of legal protection for both parties.

No collateral means no need for a Promissory Note: Regardless of whether a loan is secured (with collateral) or unsecured (without collateral), a Promissory Note is advisable. It clarifies the repayment terms and offers legal protection to the lender.

Non-payment on a Promissory Note has no real consequences: Failing to meet the terms of repayment can have serious legal and financial consequences for the borrower, including damage to credit scores, collection actions, and even legal judgment requiring repayment.

Electronic signatures aren't valid on Promissory Notes: This is no longer the case in many jurisdictions. Electronic signatures are increasingly recognized as legally valid, provided they meet certain requirements and both parties agree to their use.

Understanding these misconceptions about Promissory Notes can help individuals navigate their use more confidently and effectively, ensuring that all parties are protected and the terms of the loan are clearly understood.

Key takeaways

When dealing with a Promissory Note form, understanding the basics is crucial for both the borrower and the lender. This document is not just a formality; it's a binding legal agreement that outlines the terms under which money is borrowed and repaid. Here are some key takeaways to consider:

- Details Matter: Every Promissory Note must include detailed information about the loan's amount, interest rate, repayment schedule, and the consequence of non-payment. Vagueness leads to issues down the line, so clarity is critical.

- Legal Binding: Understand that a Promissory Note is a legal document. Once signed, it commits the borrower to repay the loan under the agreed terms. Failure to adhere to these terms can result in legal action.

- State Laws Influence Terms: The laws governing Promissory Notes vary from state to state. Interest rates, late fees, and collection costs are all subject to state regulations, which can significantly impact the terms of the note.

- Secured vs. Unsecured Notes: Decide whether the Promissory Note will be secured by collateral. Secured notes give the lender a claim to specific assets of the borrower if the loan isn't repaid, offering an extra layer of protection. Unsecured notes, while riskier for the lender, are common for smaller loans or loans between individuals who have a trusting relationship.

- Keep a Record: Both the borrower and the lender should keep a signed copy of the Promissory Note. This document will serve as evidence of the loan terms and the agreement, should any disputes arise.

Properly filling out and understanding the Promissory Note is essential in ensuring that the lending process is fair and transparent for all parties involved. Remember, when in doubt, consulting with a legal professional can provide guidance tailored to your specific situation.