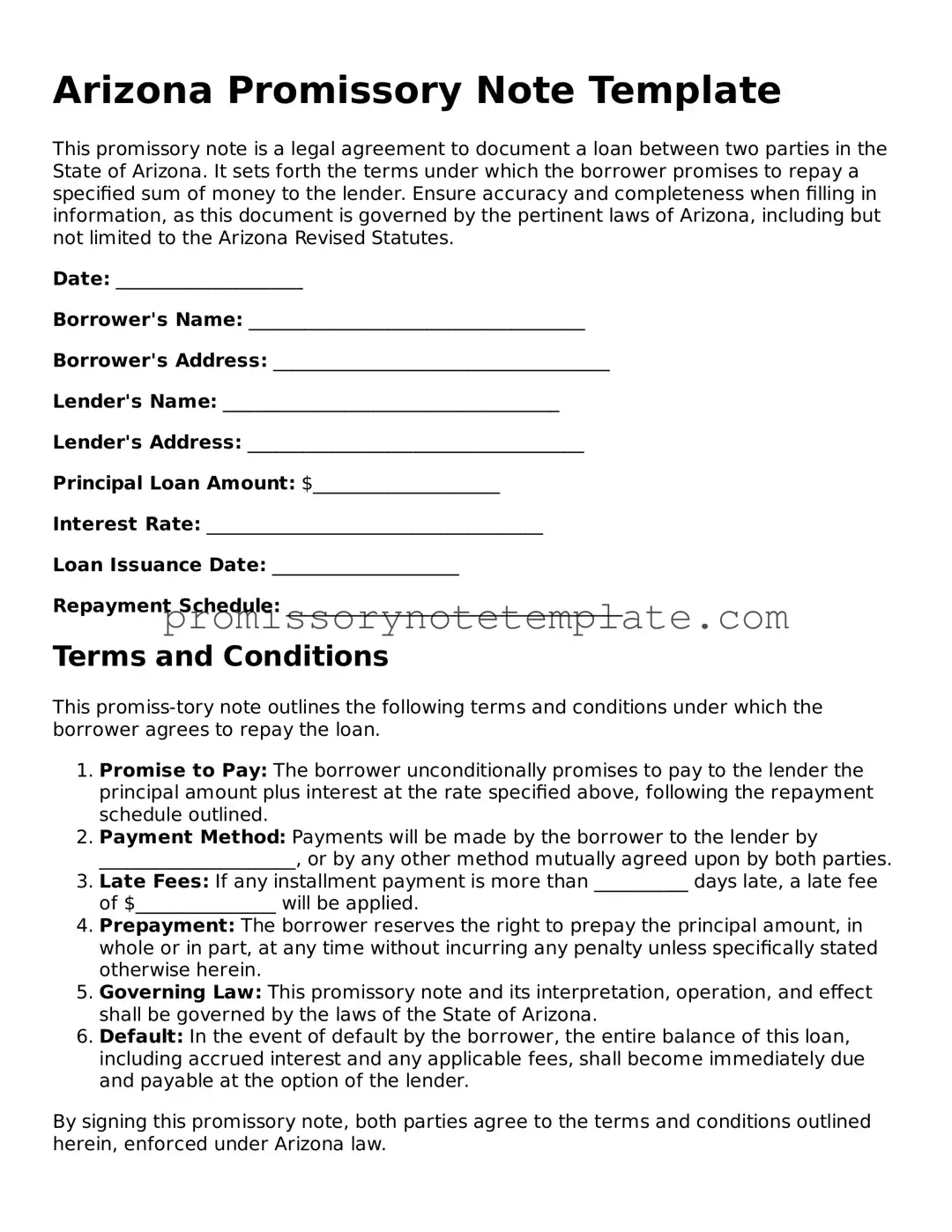

How to Use Arizona Promissory Note

When you're ready to formalize a loan agreement in Arizona, using a Promissory Note is a common approach. This document acts as a promise in writing from one party to repay another a specific amount under agreed-upon terms. While the idea of filling out legal forms can be daunting, this guide aims to make the process of completing an Arizona Promissory Note straightforward and worry-free. It's important to move through each step carefully to ensure all the details are correct and legally sound.

Steps for Filling Out the Arizona Promissory Note Form:

- Start by entering the date of the agreement at the top of the form. This should include the day, month, and year to avoid any confusion about when the terms of the note go into effect.

- Identify the parties involved. Write the full legal name of the borrower(s) and the lender(s). If there are multiple borrowers or lenders, ensure each individual's name is listed.

- Specify the loan amount. Clearly state the total amount of money being borrowed. This figure should be written in both words and figures for clarity.

- Detail the interest rate. Include the annual interest rate that will be applied to the principal loan amount. Arizona law may limit this rate, so it's wise to check current regulations to ensure compliance.

- Outline the repayment schedule. Indicate how the loan will be repaid, such as in installments or a lump sum, and specify the due dates for these payments. It's crucial to agree on a schedule that is realistic and manageable for the borrower.

- Include details about late fees. If there will be charges for late payments, describe these penalties clearly, including how much will be charged and when these fees will apply.

- Address security, if applicable. If the loan is secured with collateral, describe the collateral item(s) in detail to ensure there's a mutual understanding of what is being pledged.

- Signatures. Both the borrower(s) and lender(s) must sign the form. It's also a good practice to have the signatures witnessed or notarized to authenticate the document.

Filling out an Arizona Promissory Note with accuracy and attention to detail is the first step in creating a clear and enforceable loan agreement. Once the form is completed, it's advisable for both the borrower and lender to keep a copy for their records. This ensures that both parties have a reference for the terms agreed upon, which can help prevent misunderstandings and provide legal protection if disputes arise. Following these steps diligently will help create a solid foundation for financial transactions between individuals or entities, making the lending process smoother and more transparent for everyone involved.