How to Use Arkansas Promissory Note

Filling out the Arkansas Promissory Note form is a straightforward process that formalizes a loan agreement between two parties. It's a legal document that outlines how much money is being borrowed, the interest rate, repayment schedule, and what happens if the loan is not repaid. This ensures that both the borrower and the lender are on the same page and legally protected. Carefully completing this form is very important to avoid any potential misunderstandings or legal issues in the future. Let's go through the steps needed to fill it out properly.

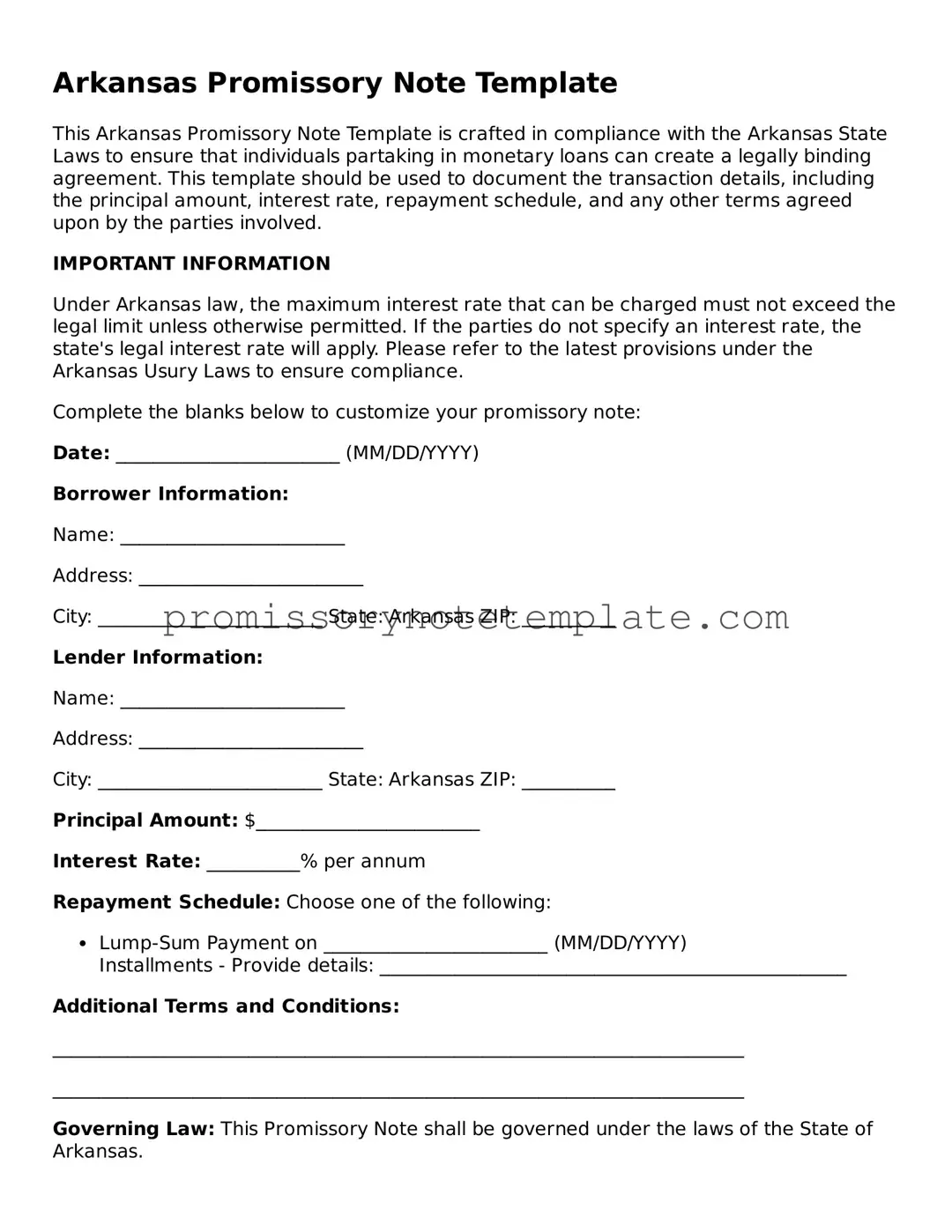

- Gather the necessary information, including the full names and addresses of both the lender and the borrower, the principal loan amount, interest rate, and the loan's repayment schedule.

- Enter the date the promissory note is being created at the top of the form.

- Write the full legal names and addresses of the borrower and lender in the designated sections. Make sure to double-check the spelling and accuracy.

- Specify the principal amount of the loan in words and then in numbers to ensure clarity. This is the amount of money being borrowed before any interest.

- Detail the interest rate agreed upon. This rate should be an annual percentage of the principal.

- Describe the repayment terms. This includes how often payments will be made (monthly, quarterly, etc.), the amount of each payment, and the duration of the loan. Also, mention any provisions for late payments or penalties.

- Include any agreed-upon collateral. If the loan is secured, describe the asset being used as security for the loan.

- If there are any cosigners to the promissory note, their information should be added. A cosigner agrees to take responsibility for the loan if the primary borrower fails to repay.

- Both the borrower and the lender must sign and date the bottom of the promissory note, making it a legally binding agreement. Witness signatures may also be required, depending on local laws.

- Make copies of the signed promissory note. Give one to the borrower, keep one for the lender, and consider having a third copy kept by a neutral third party for safekeeping.

Once the form is filled out and signed, the agreement is considered active. The borrower is now obligated to repay the loan under the terms outlined in the promissory note. Both parties should keep their copies of the document in a safe place for the duration of the loan period. Should any issues arise with the loan, this document will serve as the primary evidence of the terms agreed upon by both parties.