How to Use California Promissory Note

After deciding to lend or borrow money in California, it's crucial to document the terms of the agreement in writing using a Promissory Note form. This form legally details how the borrower will repay the debt, including any interest and the payment schedule. Completing this form accurately ensures all involved parties understand their responsibilities and can protect their interests in case of disputes. Follow these steps to ensure you fill it out correctly.

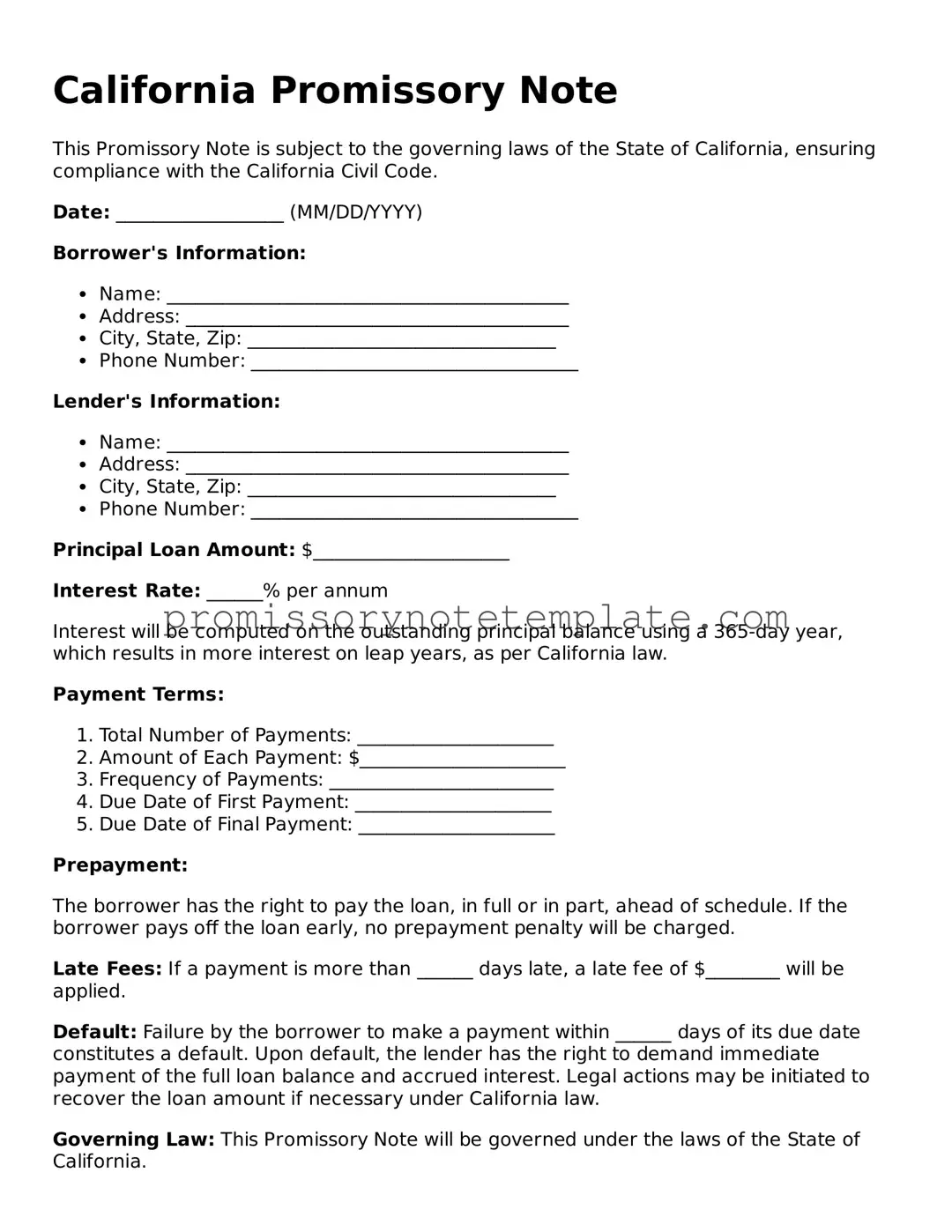

- Gather Required Information: Before starting, both the lender and borrower should collect essential details such as their full legal names, addresses, the loan amount, the interest rate, and the repayment schedule.

- Enter the Date: At the top of the form, write the current date to mark when the agreement goes into effect.

- Identify the Parties: Clearly write the full legal names and addresses of the borrower and the lender in the designated sections.

- Document the Loan Amount: Specify the principal amount of money being loaned, without including the interest, in the section labelled "Principal Amount."

- Detail the Interest Rate: Enter the annual interest rate that the borrower agrees to pay. This rate must comply with California's usury laws.

- Outline Repayment Terms: Specify the loan's repayment schedule, including the start date of payments, the amount of each payment, and how often payments will be made (monthly, weekly, etc.). Also, indicate the final due date for the loan's full repayment.

- Include Late Fees: If applicable, describe any late fees the borrower will incur if a payment is made after its due date. Include how many days after a missed payment a fee will be charged and the amount of the fee.

- Address Early Repayment: State whether the borrower can pay off the loan early and if there are any penalties for doing so.

- Signatures: After thoroughly reviewing the document to ensure all information is accurate and complete, both the borrower and the lender must sign and date the Promissory Note. It's a good practice to have the signatures notarized, although not required.

- Witnesses: If applicable, have one or two neutral parties sign the document as witnesses. Their contact information should also be included, though this step is optional. mphasize>

- If necessary, consult with a legal advisor to ensure that the terms of the Promissory Note comply with California laws and that your interests are protected.

Once all parties have signed the Promissory Note, make sure both the borrower and the lender receive a copy of the document for their records. Keeping this document safe is essential for future reference, especially if disagreements or legal issues arise regarding the loan. Remember, this Promissory Note serves as a binding legal agreement; therefore, understanding and adhering to its terms is crucial for both parties involved.