How to Use Colorado Promissory Note

Upon deciding to engage in a financial agreement in Colorado, utilizing a promissory note form can streamline the process of documenting the loan terms and repayment schedule. This form, legally binding, ensures that both the borrower and the lender have a clear understanding of their obligations. Proper completion of the form is not just a formality but a crucial step in safeguarding the interests of both parties involved. Following step-by-step instructions can assist in filling out the form accurately, ensuring all necessary details are covered.

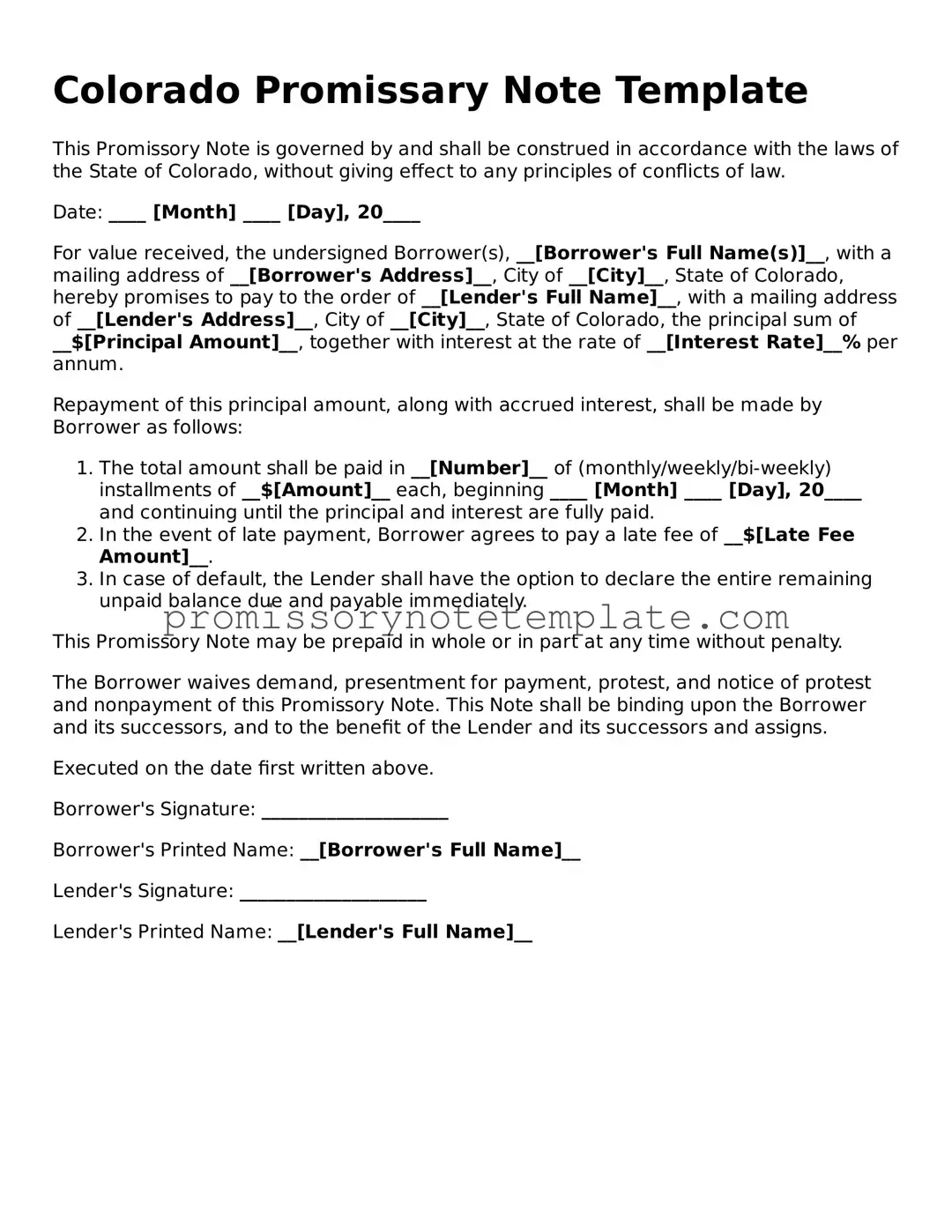

- Begin by entering the date on which the promissory note is being created, at the top of the document.

- Fill in the full name and address of the borrower, ensuring it matches their legal identification.

- Insert the full name and address of the lender, again, verifying accuracy against legal documents.

- Specify the principal loan amount in U.S. dollars, without including interest.

- Detail the interest rate per annum, adhering to Colorado's legal limits to avoid usurious rates.

- Choose the loan repayment structure (e.g., lump sum, installment) and specify the schedule, including due dates.

- Include any relevant information about late fees, specifying the amount and the grace period before they are applied.

- Detail the collateral, if any, being used as security for the loan. This section is crucial if the promissory note is secured.

- Both the borrower and lender must sign and date the form at the bottom, making it a legally binding agreement.

- If applicable, have the document notarized to add an extra layer of legal protection and authenticity.

Once the form is filled out and signed, it's important to distribute copies to both the borrower and the lender, retaining it within their records. This completed document not only serves as a commitment to repay the loan but also acts as evidence of the financial transaction, which can be crucial for both parties in case of disputes or legal proceedings. Regular reference to the promissory note throughout the loan term can help in maintaining transparency and trust between the borrower and lender.