How to Use District of Columbia Promissory Note

Filling out the District of Columbia Promissory Note form is a crucial step in formalizing a loan agreement between a borrower and a lender within the jurisdiction of Washington D.C. This document ensures there's a legally binding record of the loan's terms and conditions, including repayment. It's important to complete this form with accuracy and attention to detail to protect the interests of both parties involved. Following the next steps will guide you through the process, ensuring that all necessary information is properly documented.

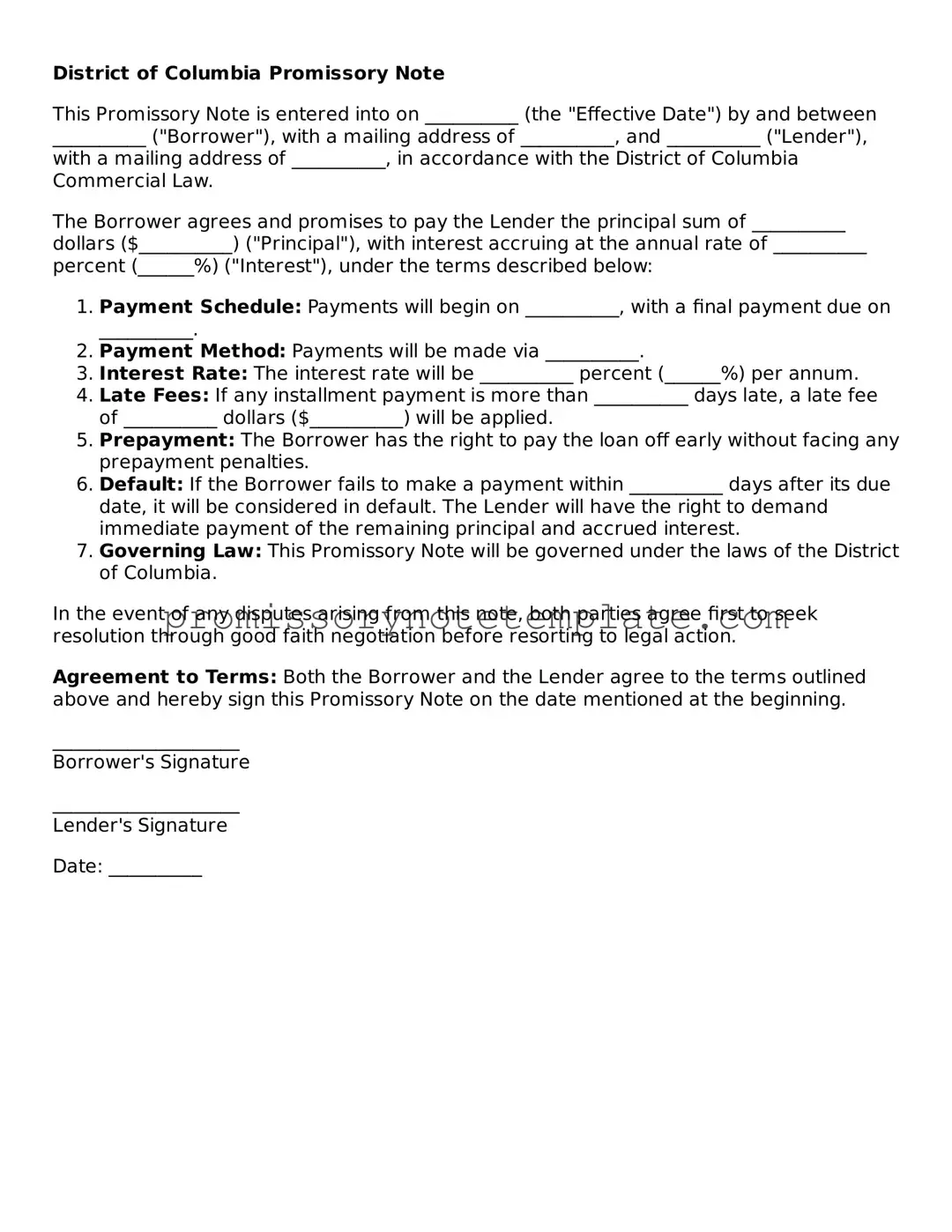

- Enter the date the promissory note is being created in the format: Month, Day, Year.

- Write the full legal name of the borrower and the lender, along with their complete addresses, including the city, state, and ZIP code.

- Specify the principal amount of the loan in U.S. dollars.

- Detail the interest rate per annum, ensuring it complies with the legal maximum in the District of Columbia. If the loan is interest-free, this should also be stated clearly.

- Describe the repayment schedule. Include the start date of payments, the frequency of payments (monthly, quarterly, etc.), the amount of each payment, and the due date for the final payment. If there are any specific conditions for early repayment, make sure to include those as well.

- Include a clause about late fees, specifying the amount to be charged and when it is applicable after a missed payment deadline.

- If the loan is secured by collateral, describe the collateral in detail to ensure there's a clear understanding of what is securing the loan.

- Both the borrower and lender must sign and date the form. If there are co-signers, they should also sign and date.

- It's advisable to have the signatures notarized to authenticate the document further, although this step may not be mandatory.

Once the District of Columbia Promissory Note form is fully completed and signed, it's crucial to distribute copies to all involved parties. The original document should be kept in a safe and secure location. This form is a binding agreement, and maintaining duly completed and accurate records will ensure that both borrower and lender are protected in the case of discrepancies or disputes regarding the loan.