How to Use Hawaii Promissory Note

When you’re getting ready to fill out a Hawaii Promissory Note form, you’re essentially preparing a written promise to pay back a sum of money borrowed. This document is key in lending situations, giving both the lender and the borrower clear terms about the loan’s repayment. Understanding what each section requires can ensure the promissory note holds up in the legal sense and helps prevent future misunderstandings between the parties involved.

- Start by entering the date the promissory note is being created at the top of the document. Make sure the date format follows the local standards in Hawaii.

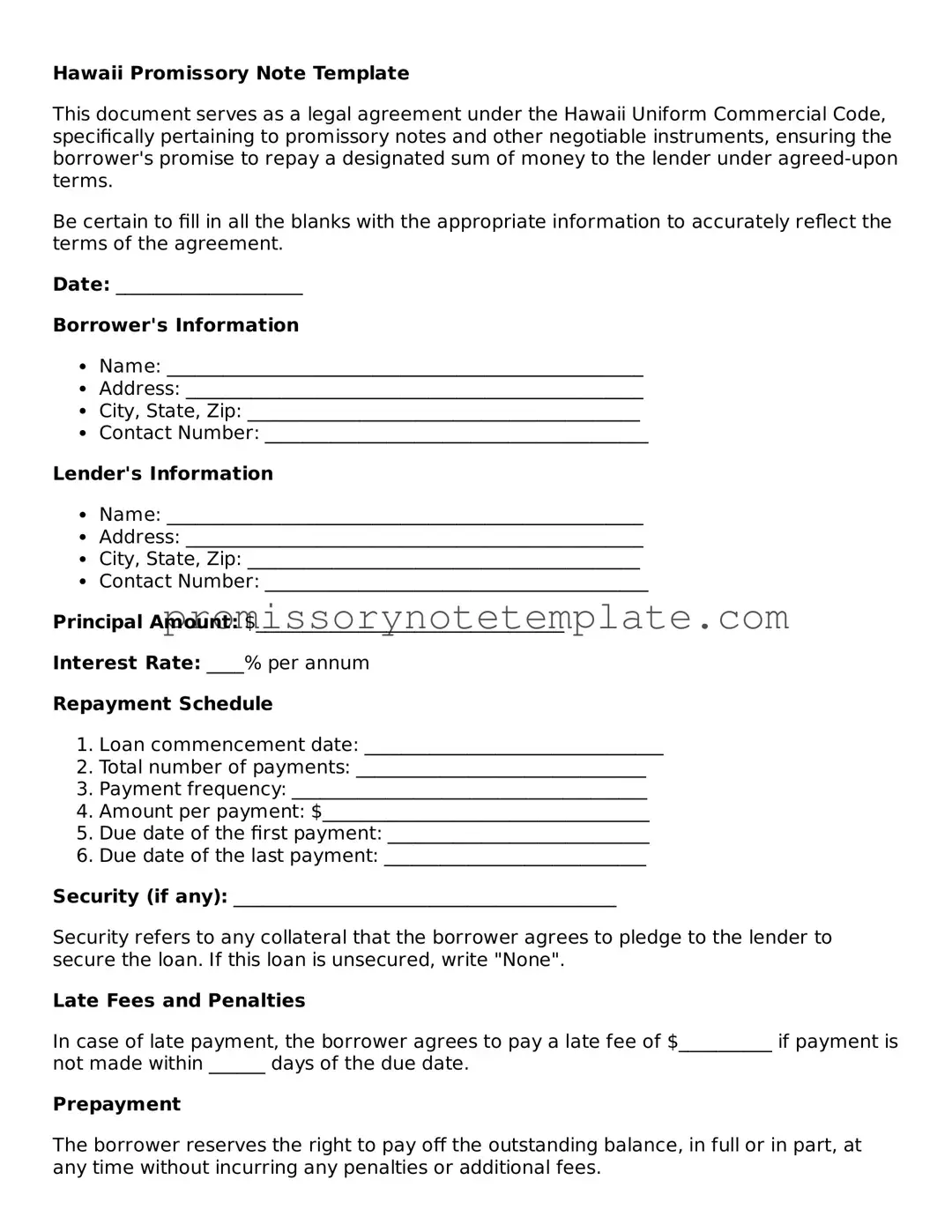

- Write the full legal name of the borrower (the person who is borrowing the money) and their full address, including the city, state, and zip code.

- Enter the full legal name of the lender (the person or entity lending the money) along with their complete address.

- Specify the amount of money being borrowed. This should be written in both words and numbers to avoid any potential confusion.

- Detail the interest rate that will be applied to the borrowed money. In Hawaii, the interest rate must comply with state regulations, so it’s important to verify the current legal maximum before filling this out.

- Outline the repayment plan. Include specific dates, amounts, and any other conditions related to how the borrower is expected to repay the loan. This section can detail whether payments will be monthly, quarterly, etc., and whether there will be a final lump-sum payment.

- If there are any collateral items that the borrower is using to secure the loan, describe them in this section of the form. Include detailed descriptions of the collateral to ensure clarity.

- Both the borrower and the lender should sign and print their names at the bottom of the document. Witness signatures may also be required, depending on local laws in Hawaii.

- Date the signatures to finalize the document. The date should reflect when the promissory note is officially completed and agreed upon.

Filling out the Hawaii Promissory Note form correctly is crucial for ensuring the legal enforceability of the loan. Both parties should keep a copy of this document for their records once it’s been completed and signed. This step-by-step guide provides a straightforward pathway to preparing your promissory note, ensuring clarity and mutual understanding between the lender and the borrower.