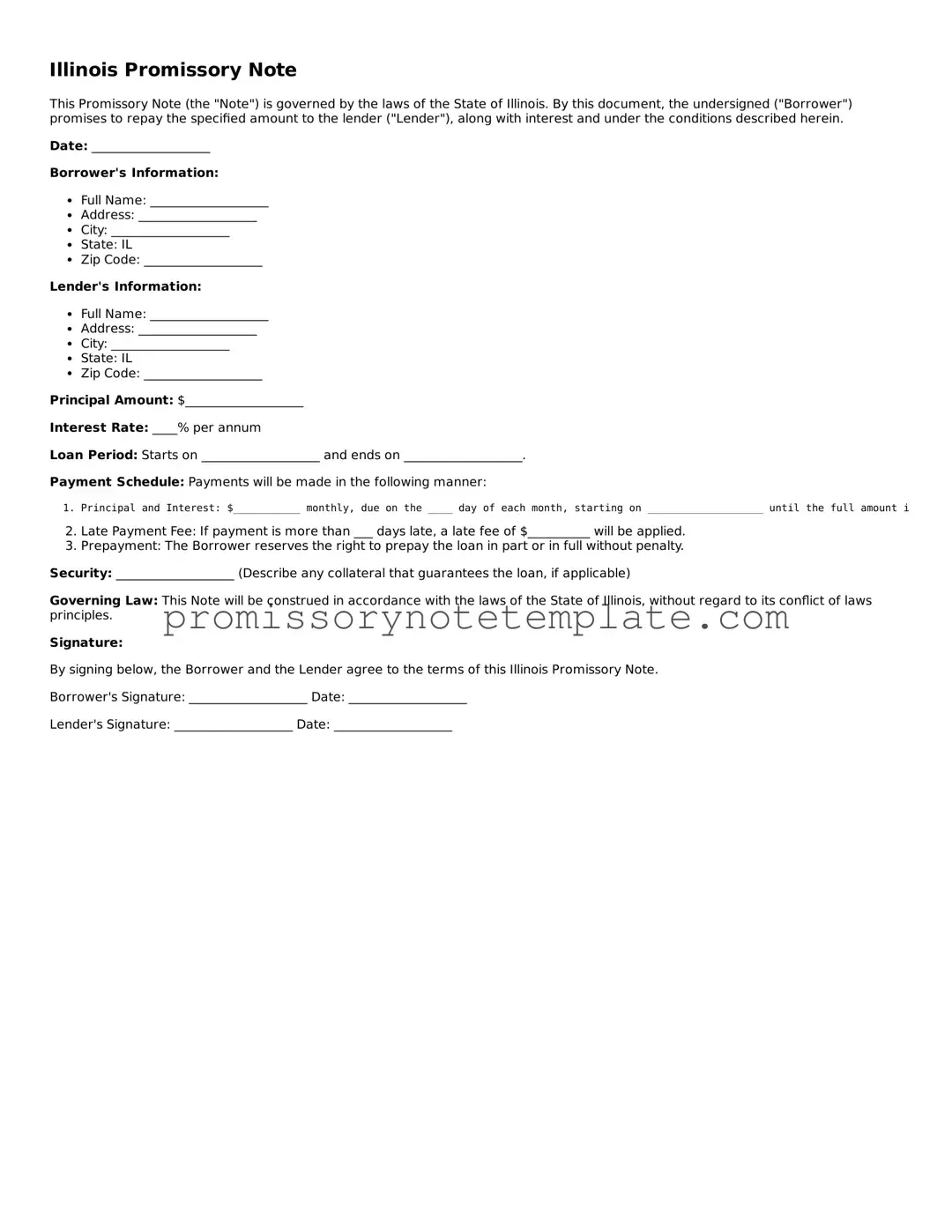

How to Use Illinois Promissory Note

Filling out the Illinois Promissory Note form is a straightforward process that requires attention to detail. This document is crucial for laying out the terms of a loan between two parties, specifying the repayment schedule, interest rate, and other essential conditions. To ensure clarity and adherence to legal requirements, it's important to complete this form accurately. Following the steps below will guide individuals through the process, from identifying the parties involved to outlining the repayment terms.

- Begin by entering the date at the top of the form. This should be the day the agreement is being made.

- Write down the full names and addresses of the borrower and the lender in the designated sections to clearly identify the parties involved.

- Specify the amount of money being lent. This should be written in both words and figures for clarity.

- Indicate the interest rate per annum. State laws may regulate the maximum allowable interest rate, so it's critical to verify this before completion.

- Choose the repayment schedule. This can be in the form of instalments, a lump sum, or on-demand payments, among other options. Select the one that best fits the arrangement between the borrower and the lender.

- Include any collateral details if the loan is secured. Clearly describe the collateral that will be used to secure the loan.

- Outline the course of action in case of default. This includes any late fees, penalties, and the period after which the loan is considered in default.

- Both the borrower and the lender must sign the form. Witnesses or a notary public may also be required, depending on state laws.

After completing these steps, it's advisable to make copies of the document for both parties. This ensures each has access to the terms agreed upon, thereby protecting the interests of both the borrower and the lender. Keeping accurate records and documentation is essential in the event of disputes or misunderstandings regarding the loan agreement.