How to Use Indiana Promissory Note

When preparing to fill out an Indiana Promissory Note form, it's important to approach the task with attention to detail. This legal document serves as a promise to pay a specific amount of money under agreed-upon conditions. Filling out the form correctly is crucial to ensuring that the obligations of the borrower and the rights of the lender are clearly defined and legally enforceable. Follow these steps to complete the form properly and to provide a solid foundation for the financial agreement between the parties involved.

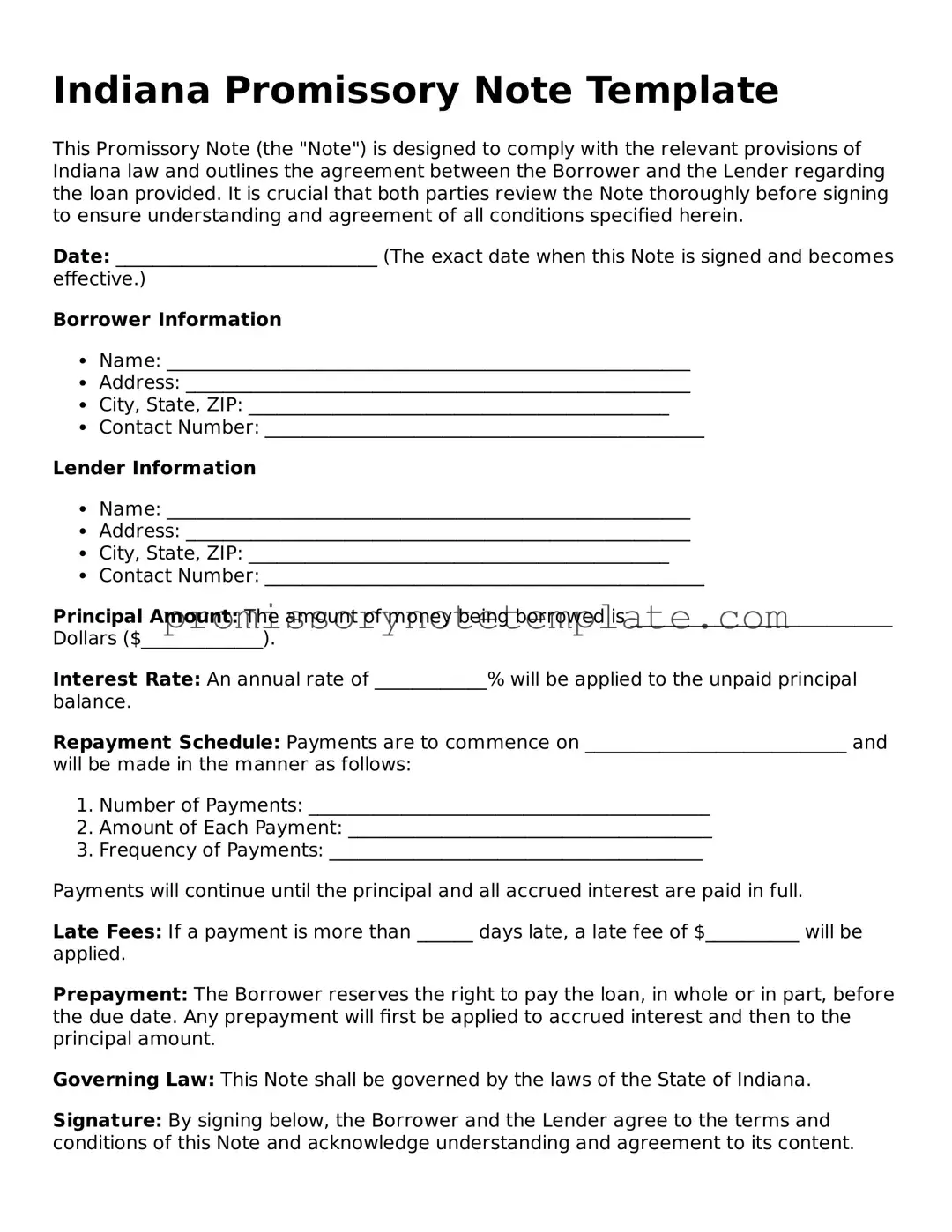

- Gather all the necessary information, including the full legal names of both the borrower and the lender, their addresses, and the amount of money being lent.

- Determine the type of promissory note — whether it is secured or unsecured. A secured note requires the borrower to pledge collateral, while an unsecured note does not.

- Specify the loan amount in words and figures to avoid any ambiguity.

- Define the interest rate. It’s essential to ensure that the interest rate complies with Indiana's usury laws to avoid any legal complications.

- Decide on a repayment schedule. Detail the frequency of payments (e.g., monthly), the amount of each payment, and the start and end dates of the repayment period.

- Include clear terms about late fees and penalties for missed payments to encourage timely repayment and to protect the lender's interests.

- Outline the conditions under which the loan must be repaid in full before the end of the term, if applicable.

- Have both the borrower and the lender sign and date the form. In Indiana, it may also be advisable to have the signatures notarized to add an extra layer of legal protection.

Once the Indiana Promissory Note form is filled out completely and signed by both parties, it becomes a legally binding document. It's important for both the borrower and the lender to keep a copy of the form for their records. Should any disagreements or disputes arise, this document will play a crucial role in resolving them. Remember, this form doesn't just outline the borrower's commitment to repay the loan; it also reinforces the lender’s rights in the agreement, making it an essential tool for clear communication and legal enforcement.