How to Use Kansas Promissory Note

Filling out the Kansas Promissory Note form is a straightforward process. This document is important as it serves as a promise to pay back a specific amount of money under agreed-upon terms. Once completed, it acts as a legally binding agreement between the borrower and the lender, detailing the loan's terms, such as the repayment schedule, interest rate, and what happens in case of default. It's crucial to accurately fill out this form to ensure clear communication and avoid any future disputes. Here’s how you can do it step-by-step:

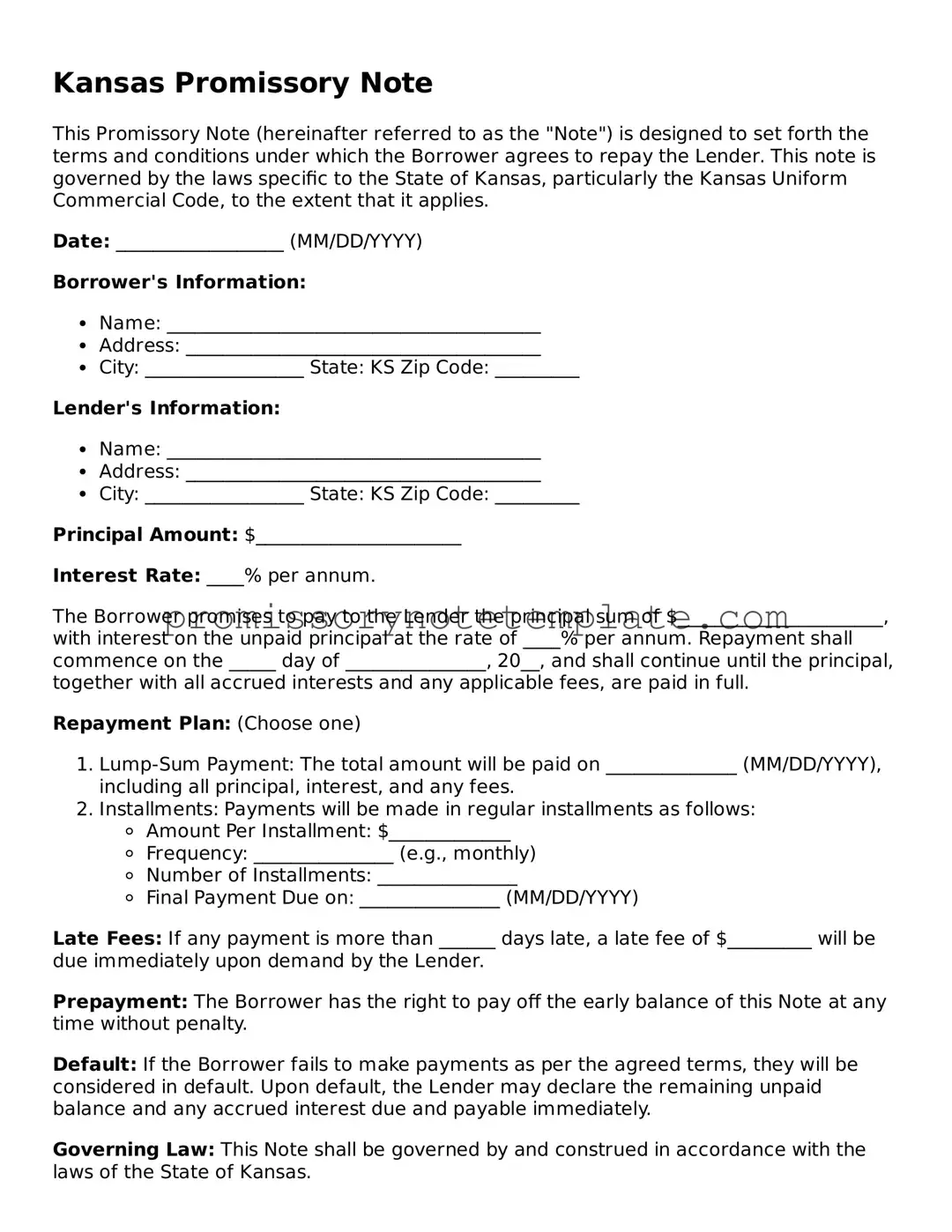

- Start by entering the Date at the top of the form. Make sure to use the format MM/DD/YYYY.

- Next, fill in the Full Name and Address of the Borrower as well as the Full Name and Address of the Lender in the designated areas.

- Enter the Principal Amount of the loan in U.S. dollars. This is the amount of money that is being borrowed before any interest is added.

- Write down the Interest Rate annually as a percentage. This is the fee charged for borrowing the money.

- Specify the Repayment Schedule. Include how often payments will be made (e.g., monthly) and the total number of payments.

- Detail the Maturity Date, which is when the loan will be fully paid off, including both principal and interest.

- If applicable, describe any Collateral securing the loan. Collateral is any asset that the lender can take if the loan is not repaid.

- Include any Co-signer information if someone besides the borrower is guaranteeing the loan.

- Detail the Late Fees policy. Indicate the amount charged if payments are made after they're due.

- State the Default terms. Explain what happens if the borrower fails to make payments or otherwise breaches the terms of the note.

- Both the Borrower and the Lender must sign and date the bottom of the form, making the agreement legally binding.

Once the Kansas Promissory Note form is filled out and signed by both parties, it’s a good practice to make copies for each party. Keep this document in a safe place as it may be needed for future reference. Should any adjustments need to be made to the agreement, ensure they are made in writing and signed by both the borrower and the lender to maintain its validity.