How to Use Kentucky Promissory Note

The process of filling out a Kentucky Promissory Note form is straightforward yet requires attention to detail to ensure that the agreement is accurately documented. This legal document formalizes the loan's terms and conditions between the lender and the borrower, including the repayment schedule, interest rate, and what happens in case of default. Filling out this form correctly is crucial for both parties involved, as it serves as a legally binding agreement that can be used for enforcement if any disputes arise regarding the loan.

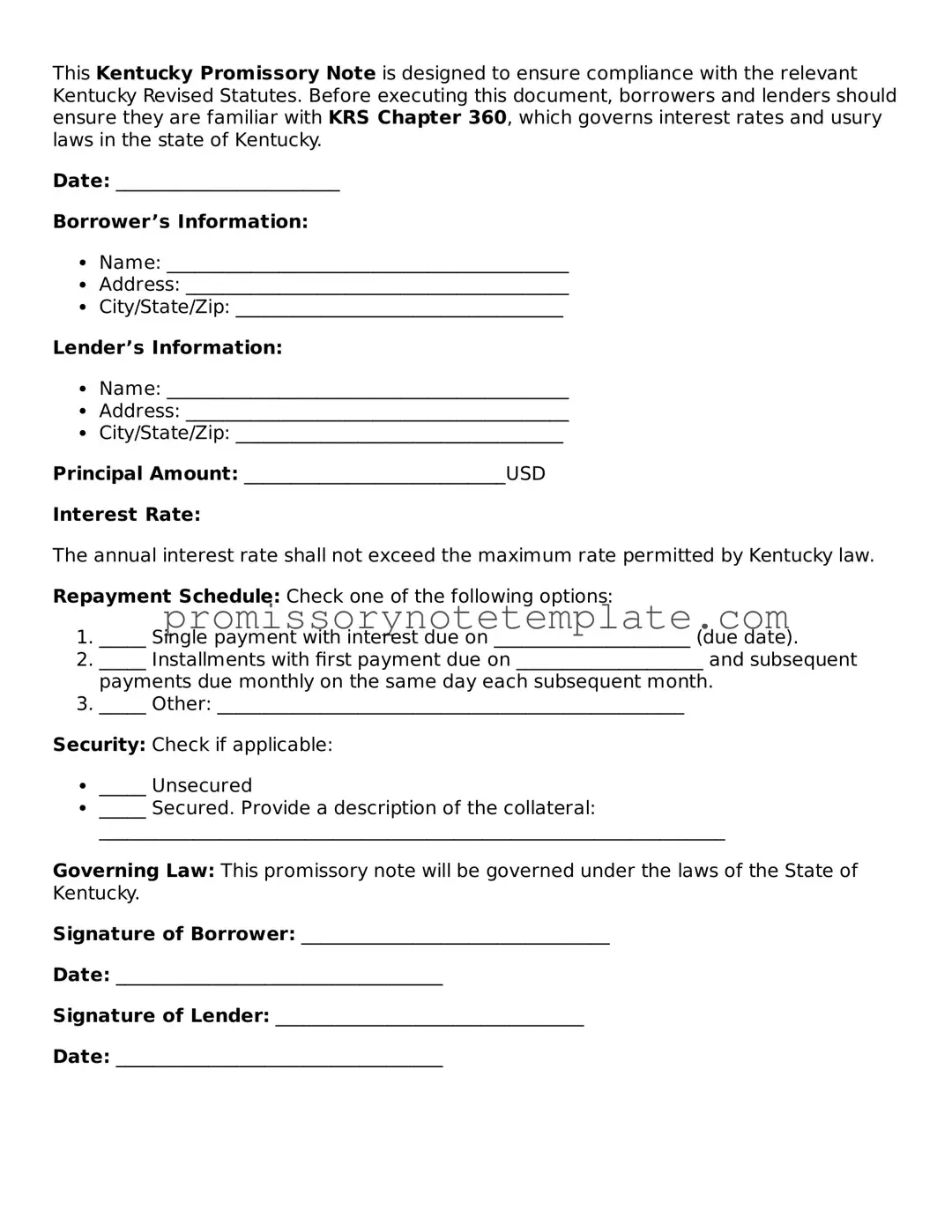

- Begin by entering the date on which the promissory note is being executed (the current date) at the top of the form.

- Write the full legal name and address of the borrower in the designated space.

- Enter the lender's full legal name and address in the space provided.

- Specify the principal amount of the loan in U.S. dollars.

- Detail the interest rate per annum. Make sure this rate complies with Kentucky's usury laws to avoid legal issues.

- Choose the type of repayment structure (e.g., installment, lump-sum, or due on demand) and clearly outline the repayment terms, including the schedule and amounts.

- For installment payments, specify the amount of each payment, the frequency of payments (monthly, quarterly, etc.), and when the first payment is due.

- Include any agreed-upon provisions for late fees, specifying the amount or percentage of the late fee and at what point after a missed payment a fee is incurred.

- If collateral is securing the loan, describe the collateral in detail to ensure there is no ambiguity about what is being used as security for the loan.

- Both the borrower and the lender must sign and date the form. Witness signatures may also be required depending on the specifics of the agreement and local law requirements.

- If applicable, have the document notarized to add an extra layer of authenticity and legal validity, although this is not always required.

Once all the steps are completed, each party should keep a copy of the signed promissory note for their records. This document is vital for maintaining transparency between the lender and the borrower and serves as a point of reference should any questions or disputes about the loan terms arise in the future.