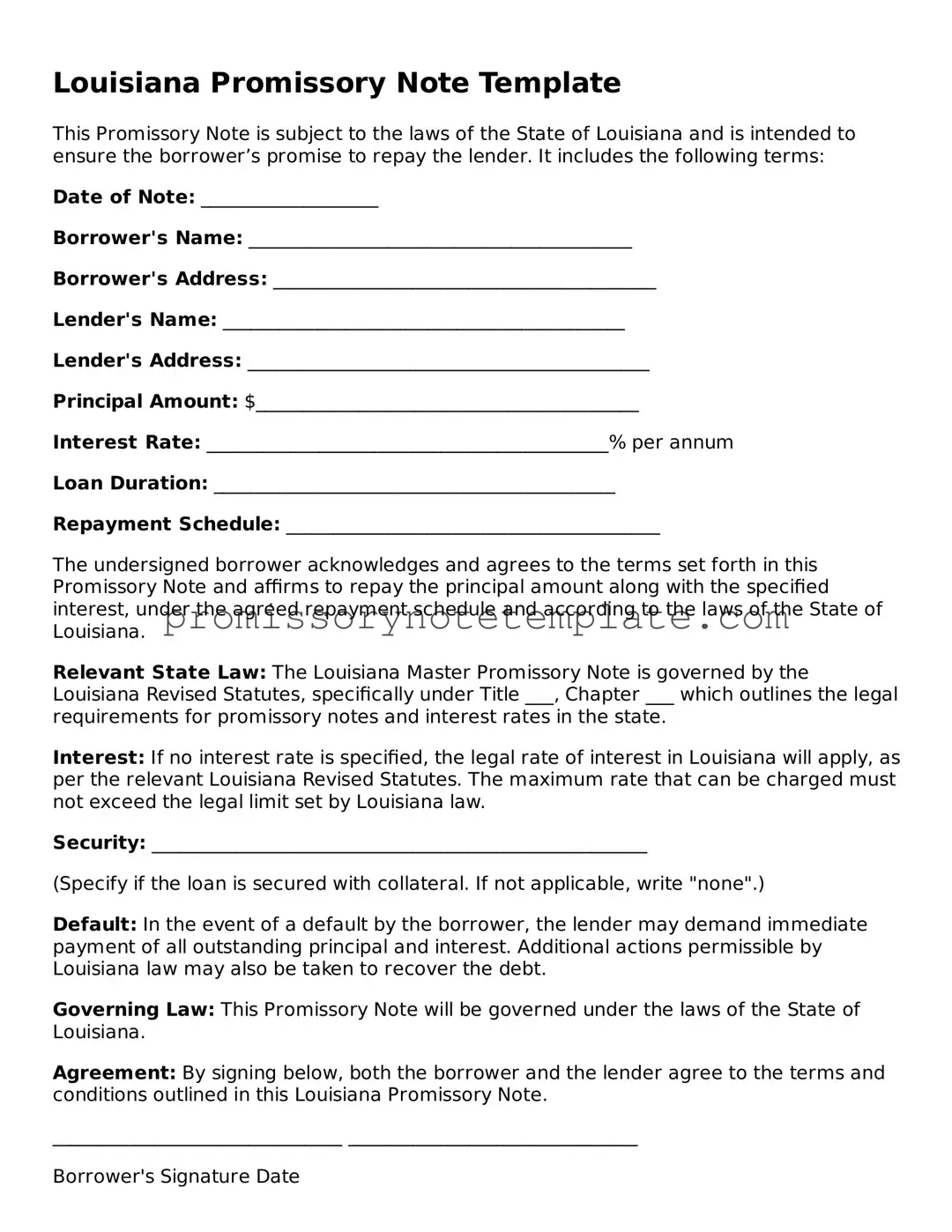

How to Use Louisiana Promissory Note

The Louisiana Promissory Note form is a pivotal document that conveys a borrower's commitment to repay a designated sum to a lender, under specified terms, within Louisiana's legal framework. This agreement, beneficial for both parties, ensures clarity on the repayment schedule, interest rate, and any collateral requirements. Completing the form correctly is crucial to its enforceability and effectiveness in establishing a clear understanding between the lender and borrower. Below are the detailed steps to accurately fill out this substantial form.

- Start by entering the date on which the promissory note is being created at the top of the form. Ensure the date format follows the local convention commonly used in Louisiana.

- Write the full name of the borrower and the lender, including their complete address with city, state, and zip code. This identifies the parties involved and establishes their commitment to the terms outlined.

- Specify the principal amount of money being loaned in US dollars. This is the amount the borrower agrees to repay under the conditions stipulated in the note.

- Detail the interest rate annually (APR) that will be applied to the principal amount. Louisiana law caps the interest rate, so verify that it complies with state regulations.

- Define the repayment schedule. This includes how often payments will be made (monthly, quarterly, etc.), the amount of each payment, and when the first payment is due. If applicable, document the final lump sum payment or balloon payment.

- Outline any collateral securing the loan. If the promissory note is secured, describe the collateral in detail, including any identification numbers or legal descriptions to ensure it is clear what is being offered as security.

- Document any co-signer information if another party is guaranteeing the loan. Include their full legal name and address, solidifying their responsibility to fulfill the obligation if the primary borrower fails to do so.

- Include the governing state law under which the promissory note will be enforced. For this document, it should specify Louisiana law.

- Both the borrower and lender must sign and date the form at the bottom. If applicable, witnesses or a notary public should also sign, depending on the requirements set forth by Louisiana law for the note to be considered legally binding.

Upon completion, this form solidifies the borrower's obligation to repay the loan under the agreed-upon terms. It acts as a legal instrument that both the lender and borrower should review carefully before signing. Once executed, it's recommended to keep multiple copies of the agreement for both parties' records and for any future reference. This ensures transparency and accountability throughout the duration of the loan repayment period.