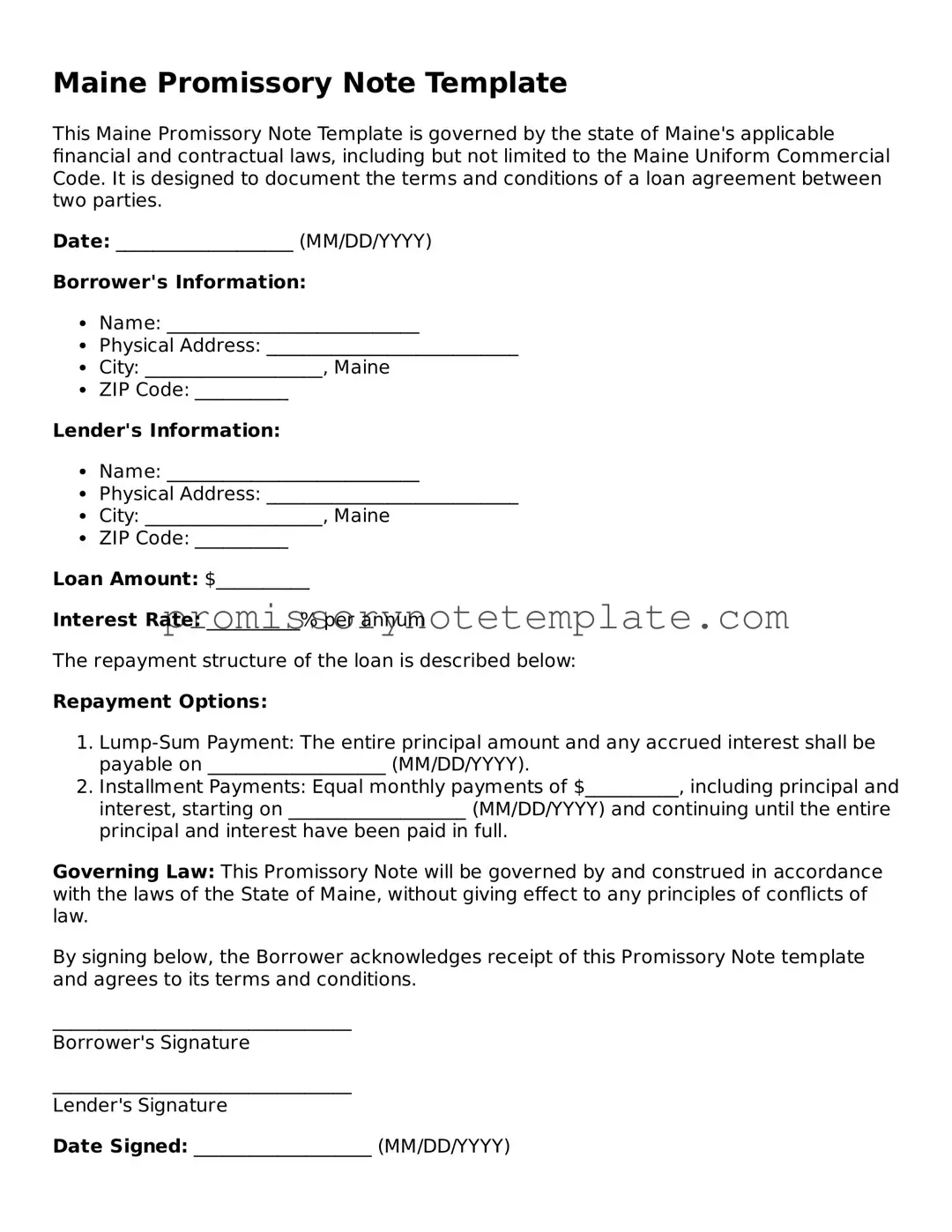

How to Use Maine Promissory Note

After you download or obtain the Maine Promissory Note form, your next step is to fill it out correctly. This document is a formal agreement where one party (the maker) promises to pay another party (the holder) a certain amount of money, either upon demand or at a specified future date, under specific terms and conditions. Completing this form accurately is crucial as it legally binds the parties to the agreement and outlines the repayment schedule, interest rate, and what happens if the payment is not made as agreed. Below are step-by-step instructions to assist you in filling out the Maine Promissory Note form.

- Enter the Date: At the top of the form, write the date when the promissory note is being created.

- Identify the Parties: Fill in the full legal names and addresses of the borrower and the lender.

- Principal Amount: Write the amount of money being loaned (the principal) in words and then in numbers.

- Interest Rate: Specify the annual interest rate. Ensure this rate complies with Maine's legal maximum interest rate, if applicable.

- Repayment Schedule: Clarify the repayment plan. Include the start date, the number of payments, frequency (e.g., monthly), and the amount of each payment.

- Security: If the loan is secured with collateral, describe the collateral in this section.

- Late Fees and Penalties: Document any fees for late payments and the conditions under which they apply.

- Co-signer Information (if applicable): If there is a co-signer, include their full legal name and address. The co-signer agrees to uphold the promise if the original borrower fails to make payments.

- Signatures: Both the borrower and the lender (and a co-signer, if one is included) must sign and date the form. Witness signatures may also be required depending on local laws.

- Governing Law: Indicate that the agreement will be governed by the laws of the State of Maine.

Once all parties have signed the promissory note and the form is completed, make sure copies are distributed to the borrower, the lender, and any co-signers involved. Retaining a copy for personal records is also advised. Properly filling out and managing the Maine Promissory Note form is essential for ensuring that all parties understand their obligations and rights under the agreement.