How to Use Maryland Promissory Note

A promissory note in Maryland, as in the rest of the country, is a legal agreement that creates a binding obligation for the borrower to repay a loan to the lender under the terms they've agreed upon. This document plays a critical role in financial transactions, ensuring there is a formal record that can be enforced in a court of law if necessary. The process of filling out a Maryland Promissory Note is straightforward but requires attention to detail to ensure all necessary information is accurately captured. Follow these steps to complete the form correctly.

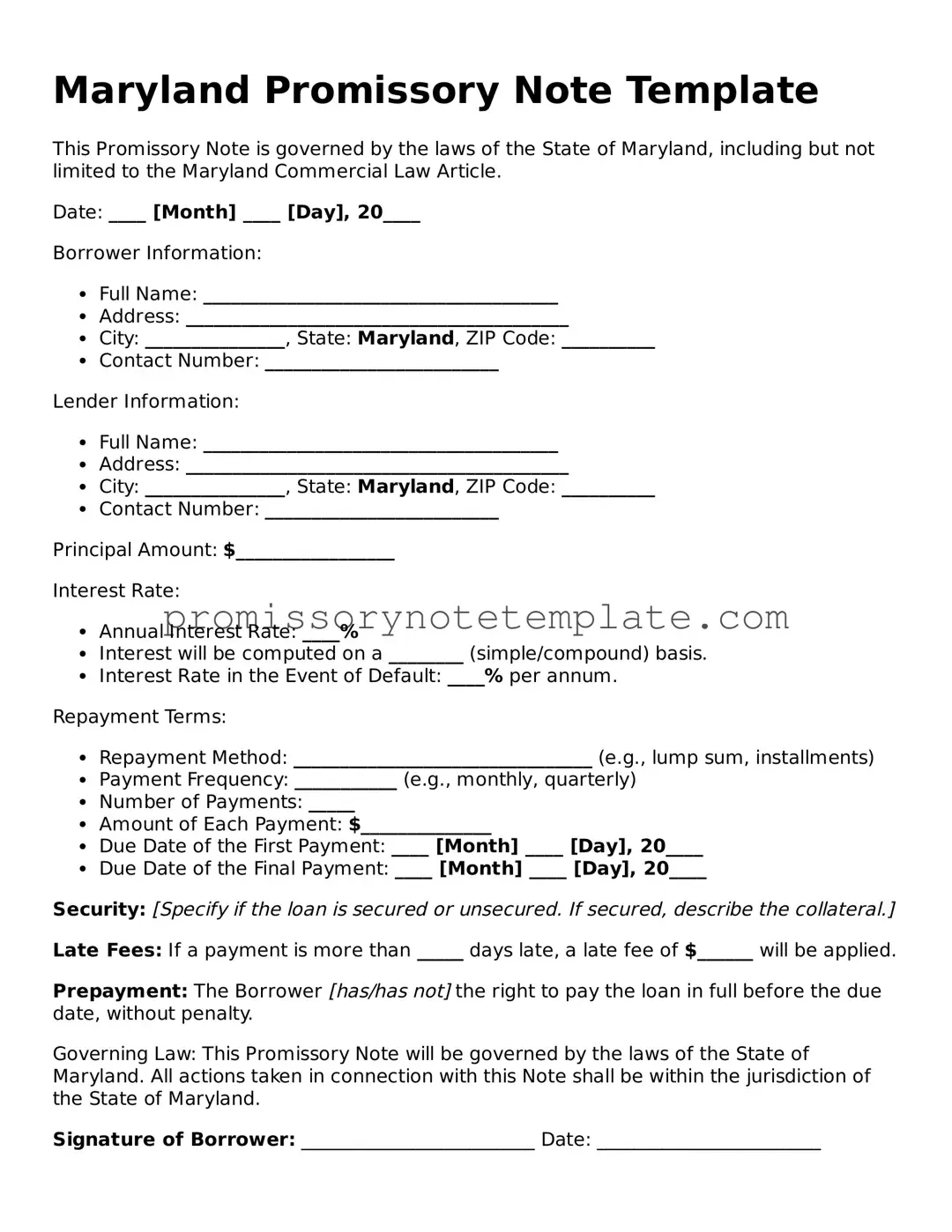

- Start by entering the date the promissory note is being created at the top of the form. This date is crucial as it marks when the agreement officially comes into effect.

- Write the full legal names of the borrower and the lender. Include addresses if the form requires it, ensuring that these details are accurate to avoid any confusion about the parties involved.

- Determine the principal amount of the loan. This is the amount of money being lent, exclusive of any interest. Enter this amount clearly in the designated space.

- Choose the interest rate. Maryland law may cap the maximum interest rate that can be charged, so it's important to ensure that the rate is in compliance with state regulations. Once confirmed, write the agreed upon interest rate on the form.

- Decide on the repayment schedule and terms. This includes when payments are due (monthly, quarterly, annually) and whether the loan will be repaid in installments or a lump sum. Clearly outline these terms in the provided section.

- Include any provisions for late fees or penalties for non-payment. This should be agreed upon by both parties and specified in the agreement to avoid potential disputes.li>

- Specify the loan's purpose if required. Some promissory notes include a section where the borrower can state the reason for the loan, though this might not be mandatory.

- Detail any collateral that will secure the loan, if applicable. Secured loans require the borrower to pledge assets as collateral, which should be clearly described in the promissory note.

- Both the borrower and the lender must sign and date the form. Witnesses or a notary public may also need to sign the form, depending on the requirements in Maryland or the preferences of the parties involved.

Once the promissoy note is fully completed and signed by all parties, it becomes a legally binding document. The borrower and lender should each keep a copy for their records. If there are any disputes or issues related to the loan, the promissory note serves as a critical piece of evidence that outlines the original terms agreed upon. It's advisable for both parties to review the entire document carefully before signing to ensure all information is correct and terms are understood. This step-by-step process ensures that the Maryland Promissory Note is filled out properly, creating a clear agreement between borrower and lender.