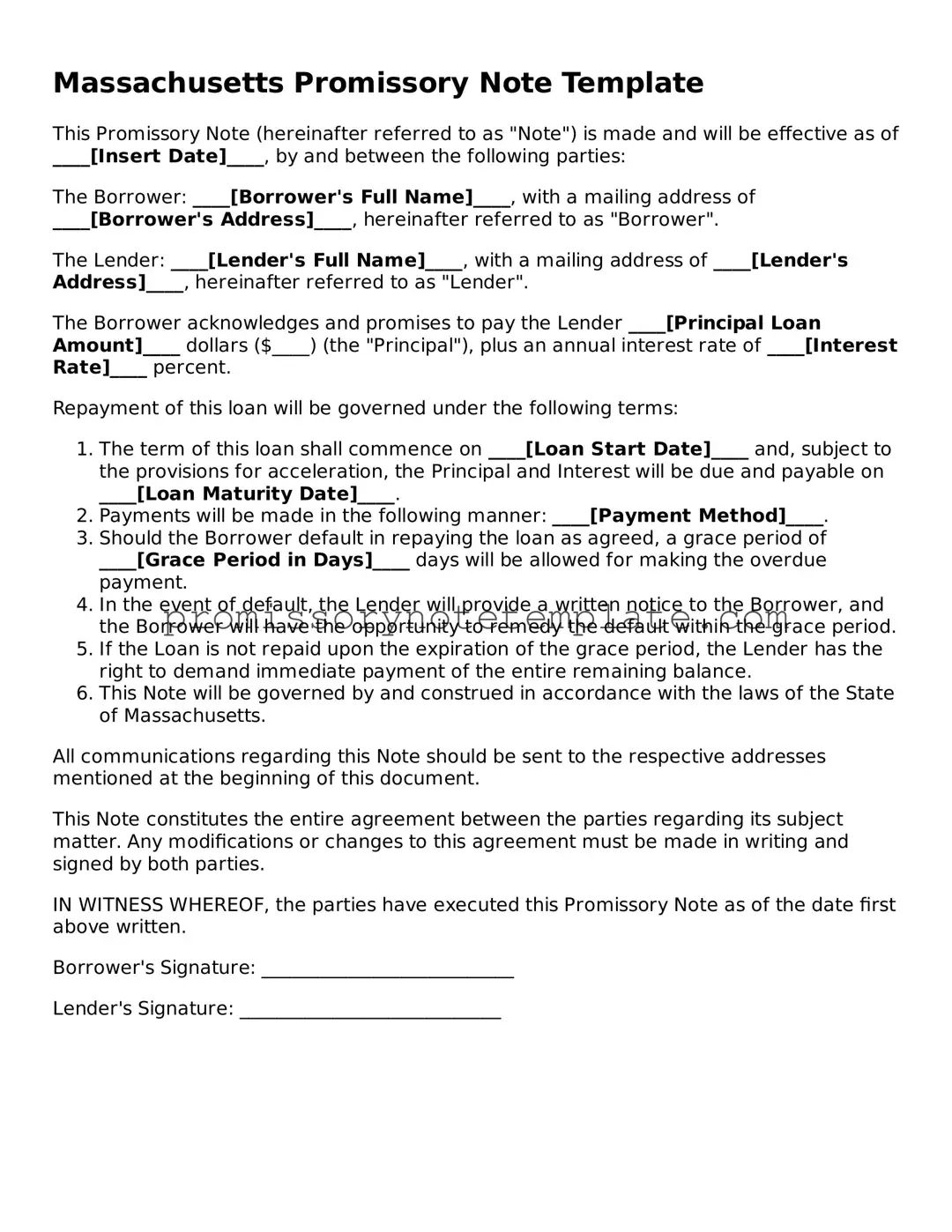

How to Use Massachusetts Promissory Note

When you're about to fill out a Massachusetts Promissory Note form, you're likely entering into an agreement where one party promises to pay another a specified sum of money, either upon demand or at a fixed or determined future date. It's a formal commitment, so it's crucial that the details are accurately recorded to protect all parties involved. Whether you're lending or borrowing money, taking the time to fill this form out carefully is a step towards ensuring a clear understanding and expectation between the parties.

Here's how to fill out the Massachusetts Promissory Note form properly:

- Start by dating the document at the top. Make sure to use the current date when you’re completing the form.

- Next, write the full legal name of the borrower - this is the person or entity who is promising to repay the money.

- Enter the full legal name of the lender - this is the person or entity who will lend the money and expects to be paid back.

- Specify the principal amount of money being loaned out in dollars. This should be the amount without interest.

- Clearly describe the terms of repayment. This includes whether the loan will be repaid in a lump sum, in regular installments, or on demand. Also, specify the due date for repayment if there is one.

- Include the interest rate per annum. In Massachusetts, make sure this rate complies with the state’s usury laws to avoid it being considered illegal.

- If collateral is being used to secure the loan, describe the property or assets clearly. This could be anything of value that the lender agrees to accept as security for the loan.

- Both the borrower and lender need to sign and date the bottom of the form. If there are co-signers, they should also sign and date the document. It’s a good practice to have the signatures notarized, although not mandatory, to add an extra layer of authenticity.

- Lastly, if there are any additional terms or conditions that the borrower and lender have agreed upon, make sure to include these in the designated section of the form.

Once you’ve completed these steps, you’ve successfully filled out the Massachusetts Promissory Note form. It’s a good idea to make copies for both the lender and borrower for record-keeping purposes. Keep the original document in a safe place as it serves as a legal document that evidence the debt. Moving forward, both parties should adhere to the terms outlined in the promissory note to ensure a smooth financial transaction and relationship.