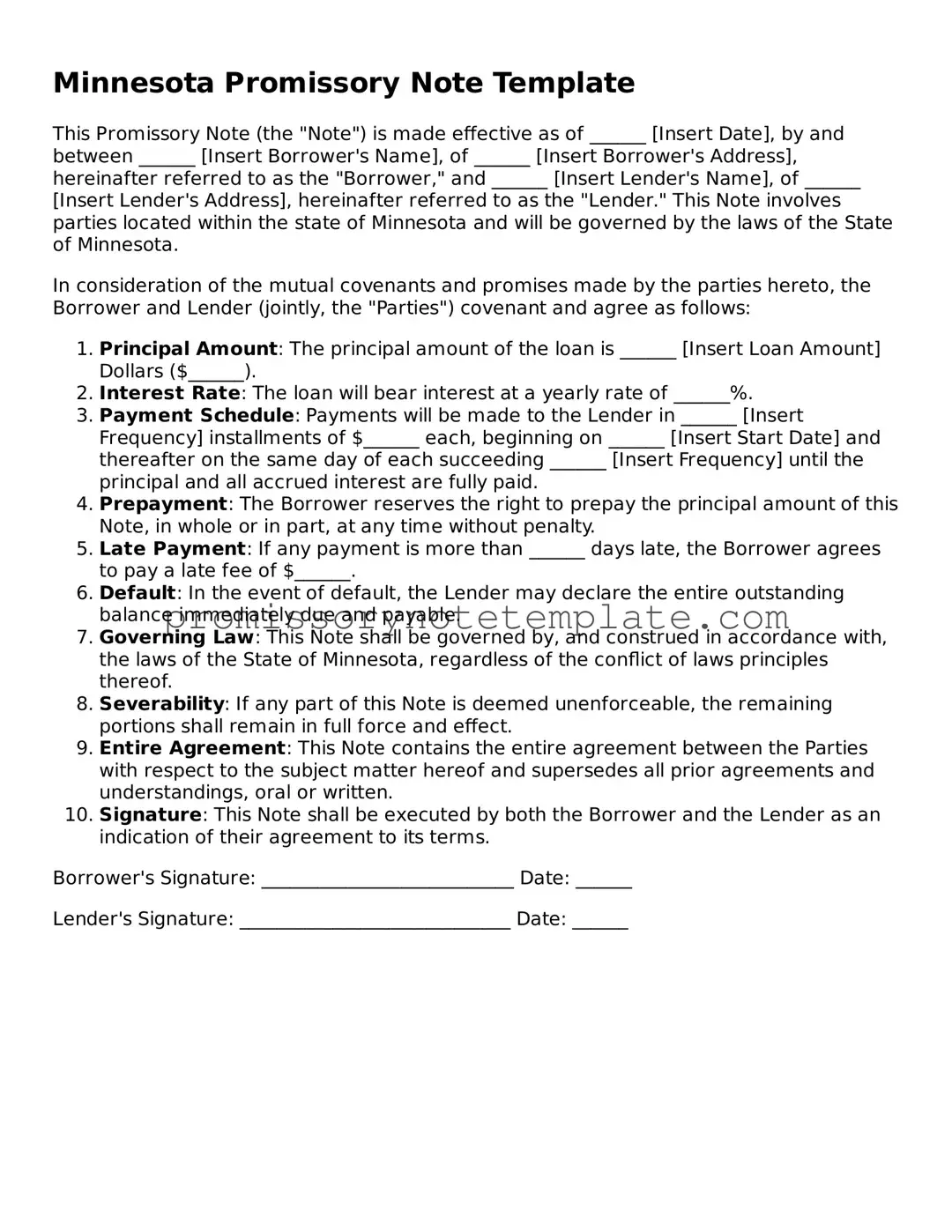

How to Use Minnesota Promissory Note

Filling out a promissory note in Minnesota is a straightforward process, though it demands attention to detail. A promissory note is a legal agreement where one party promises to pay another a specific sum of money, either at a set date in the future or upon demand. This form is essential for documenting borrowed money, and it helps in ensuring that the borrower is accountable for repayment. Below are steps designed to guide you through the process, ensuring each part of the form is completed accurately to create a binding legal document.

- Begin with the date at the top of the form. Enter the current date to record when the promissory note is being executed.

- Write down the full legal name of the borrower along with their address. This identifies who is responsible for repaying the loan.

- Include the lender’s full legal name and address. This specifies to whom the money is owed.

- State the principal amount of the loan in words and then in numbers to avoid any ambiguity about the sum being borrowed.

- Detail the interest rate per annum. Minnesota law restricts the maximum interest rate that can be charged, so ensure the rate complies with state regulations.

- Outline the repayment schedule. Specify whether the loan will be repaid in a lump sum, in regular installments, or on demand. If opting for installments, include the amount, frequency, and start date.

- Describe any security being offered for the loan, if applicable. This could include personal property, real estate, or other assets used as collateral.

- Include clauses about late fees and default provisions. Specify the amount considered late and the fees that will apply. Clearly outline the consequences if the borrower fails to make payments according to the agreed schedule.

- Both the borrower and lender must sign and print their names at the bottom of the form. The signatures make the document legally binding. Including a witness or notary signature, though not always required, can add an extra layer of legal protection.

- Make sure to keep copies of the signed promissory note for both the borrower and the lender. Keeping a record is crucial for maintaining accountability and serving as evidence of the agreement.

After completing the form following these steps, the promissory note is now legally binding. This means that the agreement has been formalized, creating a legal obligation for the borrower to repay the loan under the conditions specified. It’s important for both parties to adhere to the terms of the note and to communicate any difficulties in meeting repayment obligations as they arise. By following this guide, lenders and borrowers can ensure that their financial dealings are properly documented, paving the way for a straightforward repayment process.