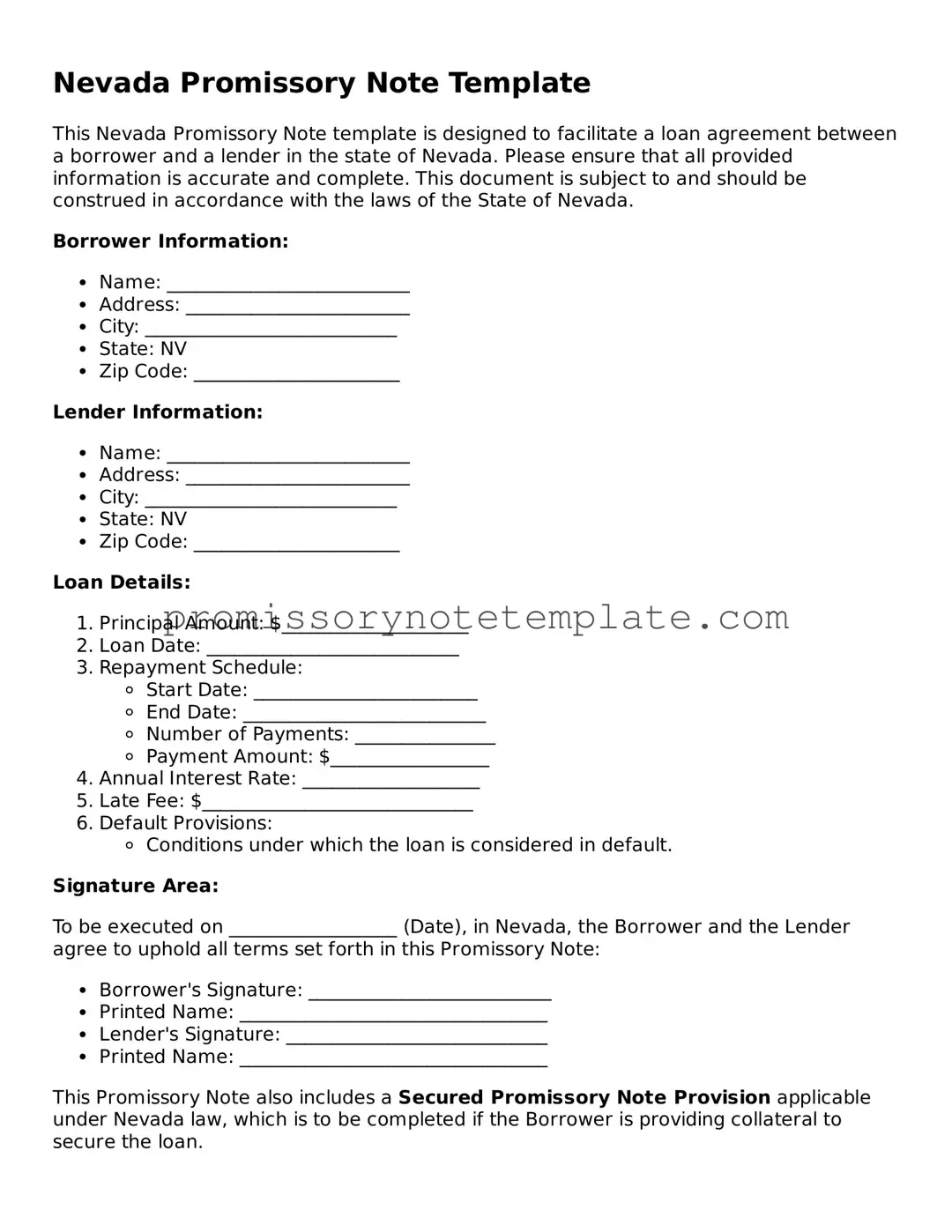

How to Use Nevada Promissory Note

When preparing to fill out a Nevada Promissory Note form, it's important to understand that this document serves as a binding agreement between a borrower and a lender. This agreement outlines the borrower's promise to pay back a specified amount of money to the lender under agreed-upon terms. The process of completing this form can be straightforward if approached with attention to detail and a clear understanding of the required information.

Here's a step-by-step guide to help ensure the document is filled out accurately:

- Start by writing the date the promissory note is being created at the top of the document. This will serve as the effective date of the agreement between the two parties.

- Enter the full legal name of the borrower along with their full address, including city, state, and ZIP code. This identifies who is responsible for repaying the loan.

- Provide the full legal name and address of the lender in the same format. This clarifies who will be receiving the repayments.

- Clearly state the principal amount of the loan in US dollars. This is the amount borrowed before any interest.

- Document the interest rate per annum that will be applied to the principal amount. It's important to ensure this rate complies with Nevada's usury laws to avoid any legal issues.

- Detail the loan repayment terms. Include how the payments will be made (e.g., monthly), the amount of each payment, and over what period. Also, specify if there's a final lump sum payment (balloon payment) at the end.

- If there are any prepayment terms that allow the borrower to pay off the loan early without penalty, make sure to include these conditions.

- Decide and document whether the loan will be secured or unsecured. If secured, describe the collateral that will be used to secure the loan.

- Both parties should read the completed document carefully to ensure accuracy and understanding of all terms and conditions.

- Finally, have the borrower and the lender sign and date the form. Witness and notary signatures may also be required, depending on the amount of the loan and the agreement between parties.

By following these steps, individuals can successfully fill out a Nevada Promissory Note form. This document then acts as a legal record of the loan agreement, helping to protect the interests of both the lender and the borrower. As with any legal document, it may be beneficial to seek legal advice or assistance to ensure that all aspects of the note meet legal requirements and that both parties understand their obligations.