How to Use New Hampshire Promissory Note

Filling out a New Hampshire Promissory Note is an important process for documenting a loan agreement between two parties. This written promise stipulates how the borrower will repay the lender, detailing the loan amount, interest rate, repayment schedule, and any other terms agreed upon. The proper completion of this document ensures clarity and legal enforceability of the financial arrangement. To accurately fill out the form, please follow the steps outlined below.

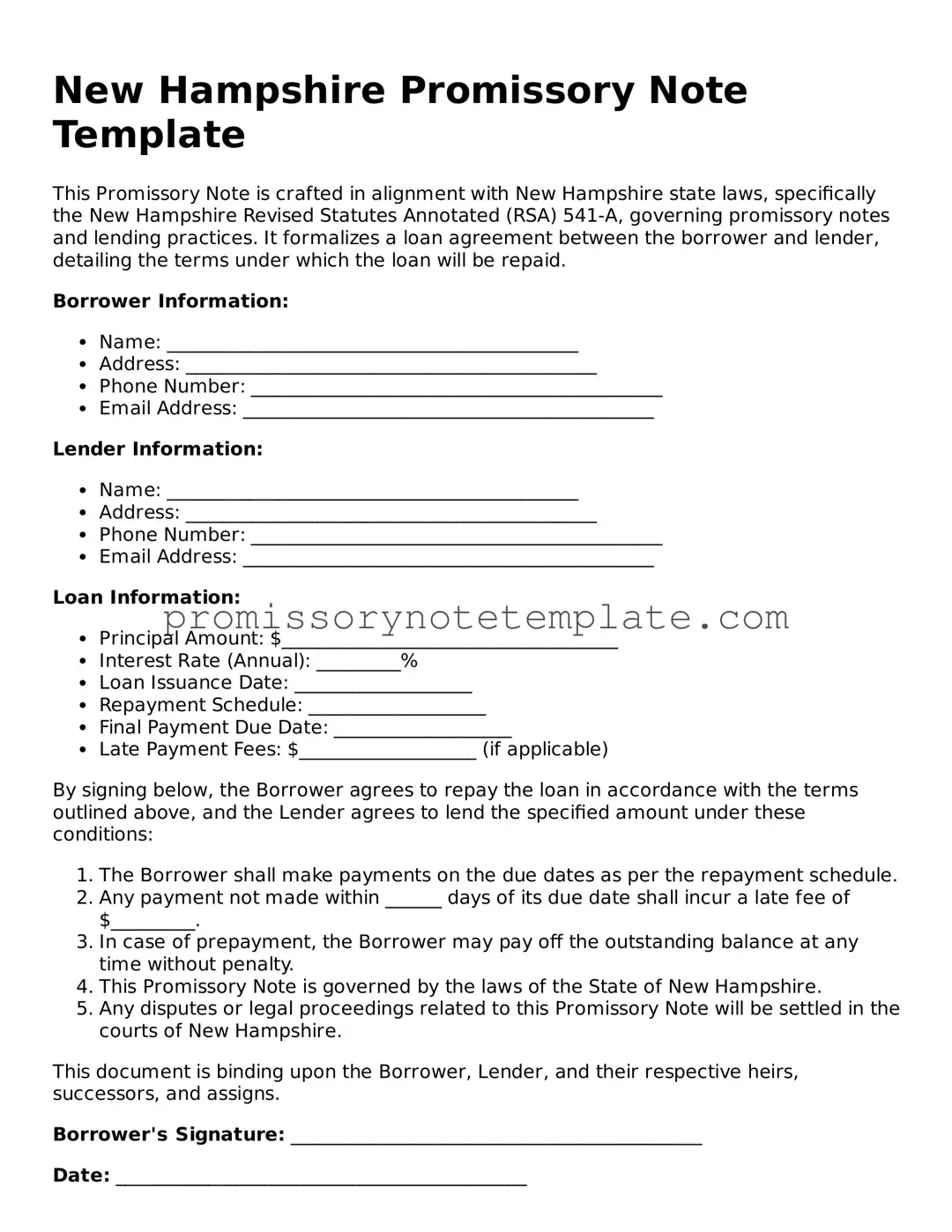

- Begin by entering the date of the agreement at the top of the form. Ensure the date reflects when the promissory note is being created.

- Write the full names and addresses of both the borrower and the lender. Include a mailing address for future correspondences related to this note.

- Specify the principal loan amount in US dollars. This should be the amount of money that the borrower agrees to repay.

- Detail the interest rate annually (APR) agreed upon by both parties. This rate should comply with New Hampshire's legal limits, if applicable.

- Describe the repayment plan. Include how often payments will be made (e.g., monthly), the amount of each payment, and when the first payment is due. Also, specify the final payment date when the loan will be fully repaid.

- Include any provisions for late payments or penalties for missed payments to ensure both parties understand the consequences.

- If collateral is being offered by the borrower as security for the loan, describe it in detail. This section is only necessary if the loan is secured.

- Both the borrower and the lender must sign and date the form at the bottom. Witness signatures may also be required, depending on local laws and regulations.

- Keep a copy of the signed promissory note for both the borrower's and the lender's records. It is crucial for maintaining a written record of the loan agreement.

After completing these steps, the New Hampshire Promissory Note will be properly filled out and can serve as a legally binding document that outlines the terms of the loan. Keeping accurate records and ensuring all parties have a copy of the signed document is key to avoiding future disputes and ensuring the agreement is upheld.