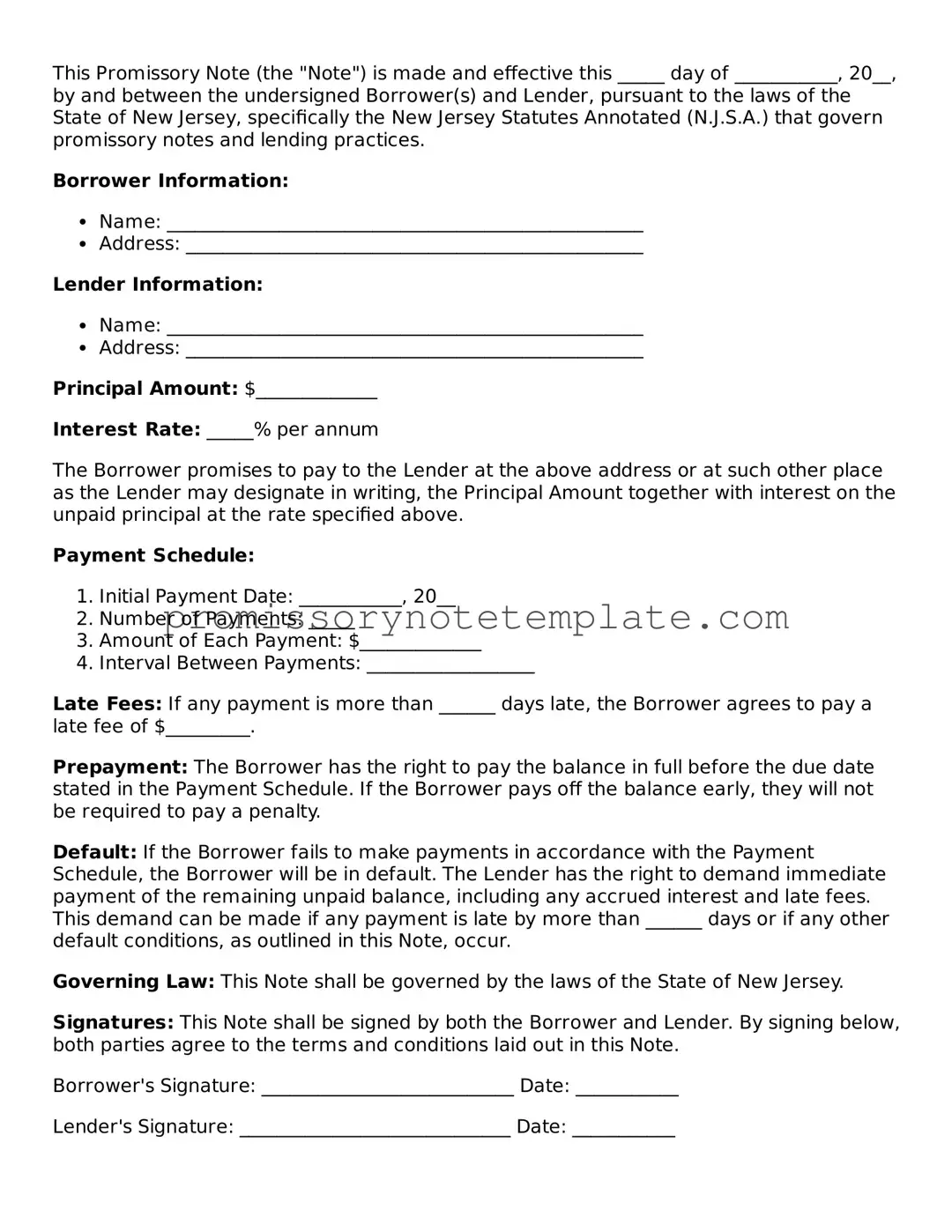

How to Use New Jersey Promissory Note

Once you have decided to enter into a loan agreement in New Jersey, completing a Promissory Note is an essential step. This legally binding document outlines the details of the loan, ensuring clarity and commitment from both the borrower and lender. The process might seem meticulous, but it's straightforward when you break it down step by step. Whether this is your first time handling a promissory note or you just need a refresher, the following instructions will guide you through each section of the form, making sure all necessary details are accurately captured.

- Begin by entering the date on which the Promissory Note is being created at the top of the form.

- Write the full legal name of the borrower and the lender, followed by their complete addresses, including city, state, and zip code.

- Specify the principal amount of the loan in U.S. dollars to make clear the total amount being lent.

- Detail the interest rate per annum. It's important that this rate complies with New Jersey's usury laws to avoid legal complications.

- Outline the repayment schedule. Include the start date, frequency of payments (monthly, quarterly, annually, etc.), and the duration or number of payments until the loan is fully repaid.

- Choose the payment method—such as cash, check, or direct deposit—and specify any details relevant to the chosen method.

- If there is any collateral securing the loan, describe the collateral in detail. This could be property or other valuable assets that the borrower pledges as security for the loan.

- Include any co-signer information, if applicable. This might be required if the borrower's creditworthiness is in doubt or if additional security for the loan is needed.

- Clearly state the conditions under which the loan must be repaid in full before the agreed-upon end date, if any.

- Articulate the terms regarding late payments or failure to pay, including any fees, penalties, or actions that will be taken.

- Both the borrower and the lender must sign and date the bottom of the Promissory Note. Witness signatures may also be necessary, depending on the legal requirements in New Jersey.

By following these steps, you'll ensure that your Promissory Note aligns with New Jersey laws and clearly documents the terms of your loan agreement. This careful attention to detail can help prevent misunderstandings and provide legal protection for both parties involved in the loan.