How to Use New York Promissory Note

Upon the decision to enter into a financial agreement in New York, where one party promises to pay another a definite sum of money, a Promissory Note form is often utilized to formalize the terms of the agreement. This tool ensures clarity and enforceability, providing a written commitment that outlines the repayment structure, interest rate, and the consequences of non-payment. The completion of this form is a crucial step in safeguarding the interests of both the lender and borrower, making the responsibilities and expectations clear from the outset. The following instructions aim to guide you through the process of filling out the New York Promissory Note form accurately.

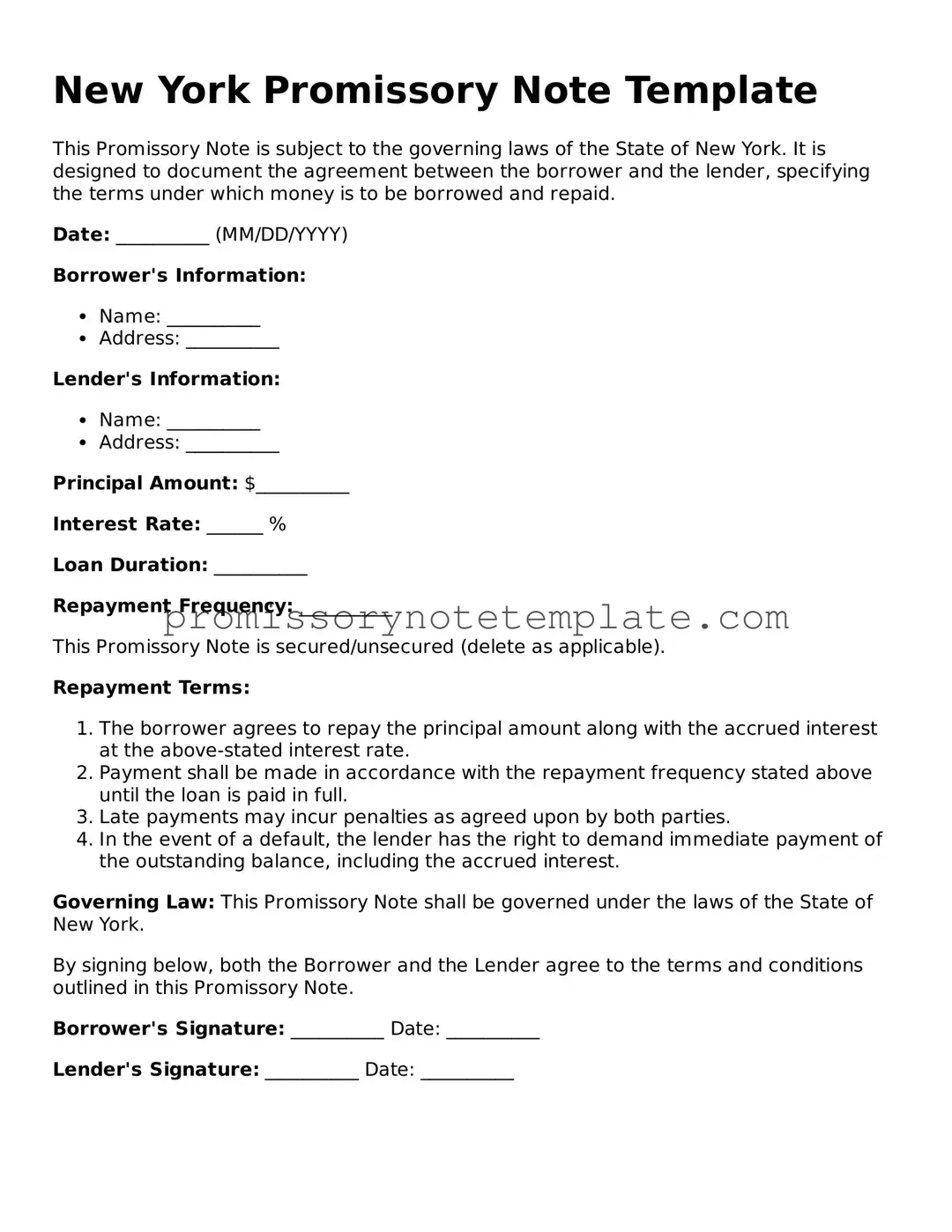

- Identify the parties: Start by clearly listing the full legal names and addresses of both the borrower and the lender. Ensure accuracy to prevent any potential disputes regarding the identities of the involved individuals or entities.

- Specify the principal amount: Indicate the amount of money being loaned (the principal) in US dollars. This should be the exact figure agreed upon by both parties.

- Determine the interest rate: Enter the annual interest rate agreed upon. This rate must comply with the usury laws of New York to ensure the note's legality.

- Choose the payment schedule: Outline the repayment schedule, including the frequency of payments (e.g., monthly, quarterly), the amount of each payment, and the start date of the repayment period. If a balloon payment is agreed upon, specify the conditions clearly.

- Detail the maturity date: Clearly state the date by which the loan should be fully repaid. This includes any final balloon payment, if applicable.

- Address prepayment: Specify if the borrower has the right to pay off the loan early without incurring penalties. If prepayment penalties will apply, describe these terms in detail.

- Governing law: Indicate that the Promissory Note will be governed by the laws of the State of New York, which will oversee any disagreements or legal proceedings related to the agreement.

- Signatures: Both the borrower and the lender must sign and date the Promissory Note. The presence of witnesses or notarization, depending on the specific requirements of the agreement, should also be noted and included at this time.

Once completed, this form serves as a legally binding document that solidifies the agreement between the borrower and lender. It is advisable for both parties to retain a copy for their records. This action ensures that, should any questions or disputes arise concerning the agreement's terms, a verifiable record is readily accessible. It is also recommended to review the form carefully before signing, and consider consulting a legal professional to ensure that the Promissory Note meets all legal requirements and adequately protects the interests of both parties involved.