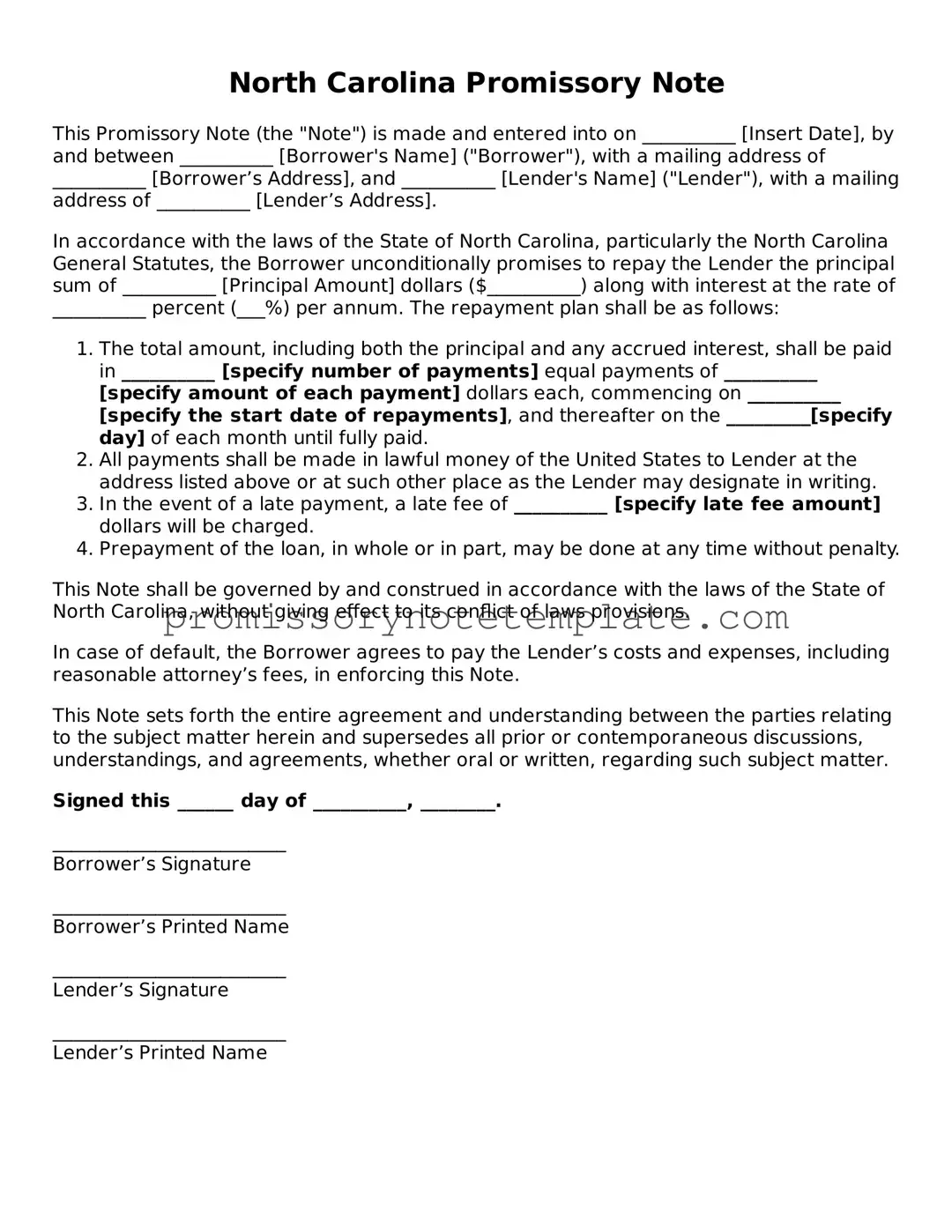

How to Use North Carolina Promissory Note

Filling out a promissory note in North Carolina is the formal way of documenting a loan agreement between two parties. It's vital to do this properly to ensure the agreement is legally binding and clear to all involved. The form will include details like the amount borrowed, the interest rate, and the repayment schedule. By completing this form, both lender and borrower have a record of the terms of the loan, which can help prevent misunderstandings and provide legal protection if any disputes arise.

- Begin by including the date the promissory note is being created at the top of the form.

- Write the full legal name of the borrower and their address in the designated sections.

- Enter the full legal name of the lender along with their address.

- Specify the amount of money being borrowed in the section labeled "Principal Amount."

- Detail the interest rate that will be applied to the borrowed amount. This must comply with North Carolina's usury laws to be enforceable.

- Choose the repayment schedule. Options typically include a lump sum on a specific date, installment payments with or without interest, or due “on demand” of the lender. Clearly write this choice on the form.

- Include specific terms regarding late fees and what constitutes default on the loan, if applicable.

- If the loan is secured with collateral, clearly describe the collateral in the provided section.

- Both the borrower and the lender must sign and date the form. Witness signatures may also be required, depending on the specifics of the agreement or the preference of the parties involved.

After having filled out the North Carolina Promissory Note form, it is crucial to keep it in a safe place. Both parties should have a copy of the document for their records. The form is a binding legal agreement, and proper safekeeping ensures it can be referenced in the future if questions or disputes arise regarding the repayment of the loan.