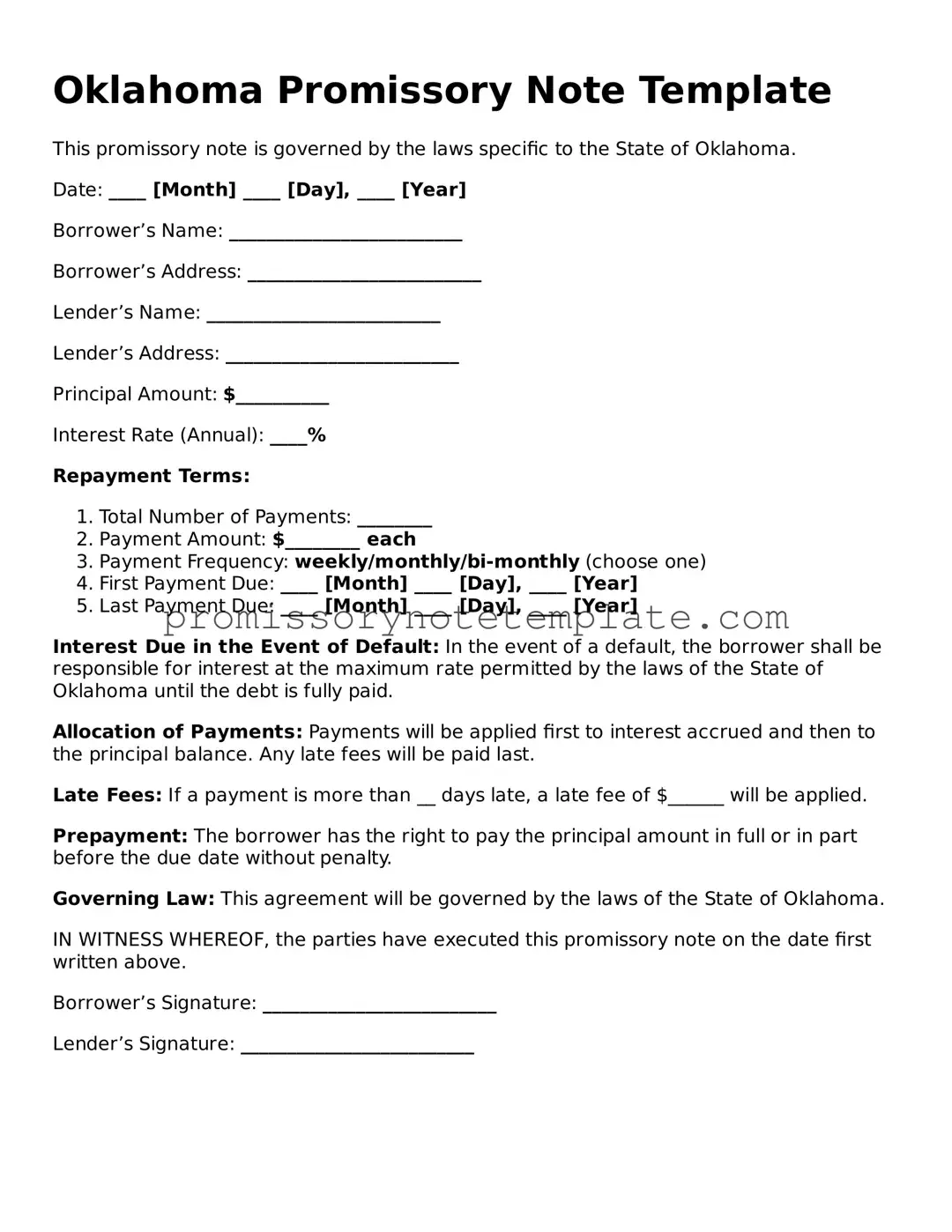

How to Use Oklahoma Promissory Note

Once both parties have agreed to the terms of a loan, completing an Oklahoma Promissory Note form is the next step. This formalizes the agreement in writing, detailing the loan's terms, repayment schedule, interest rates, and any other conditions tied to the borrowing. This document is crucial for both the lender and the borrower, as it serves as a legal record of the loan and the commitment to repay it. Filling out this form accurately is vital to ensure that all aspects of the loan agreement are clearly understood and legally binding.

- Start by entering the date of the promissory note at the top of the document.

- Write the full legal names of both the borrower and the lender, including their complete addresses.

- Specify the principal amount of the loan in US dollars.

- Detail the interest rate as an annual percentage. Ensure this rate complies with Oklahoma's usury laws to avoid illegal interest charges.

- Choose the loan's repayment structure (e.g., lump sum, installments) and clearly detail the schedule, including due dates and amounts for each payment.

- If installment payments are agreed upon, indicate whether interest will be calculated as simple or compound, and specify the frequency of interest calculations.

- Include any provisions for late fees, specifying the amount or percentage and the grace period before the fee is applied.

- Document any collateral that will secure the loan, if applicable. Describe the collateral in detail to ensure it is clearly identified.

- Add any co-signer information if someone besides the borrower will guarantee the loan. Include the co-signer's full legal name and address.

- Both the borrower and the lender must sign and date the promissory note. If a co-signer is involved, ensure they also sign the document.

- If necessary, have the signatures notarized to authenticate the identity of the signers and add an extra layer of validity to the document.

After the Oklahoma Promissory Note form is fully completed and signed by all parties, it's important to create copies for everyone involved. The signed document should be kept in a safe place, as it will be a key piece of evidence if any disputes arise or if legal action becomes necessary to enforce the repayment of the loan. Remember, a promissory note is not only a financial agreement but also a legally binding contract that obligates the borrower to repay the stated amount under the agreed terms.