How to Use Rhode Island Promissory Note

Filling out a promissory note in Rhode Island is a straightforward process, but attention to detail is crucial. A promissory note is a financial instrument that evidences a promise by one party to pay a definite sum of money to another. It's common in personal loans, business dealings, and real estate transactions. To ensure compliance and legality, the form must be filled out correctly. Following these steps will guide you through the completion of the Rhode Island Promissory Note form.

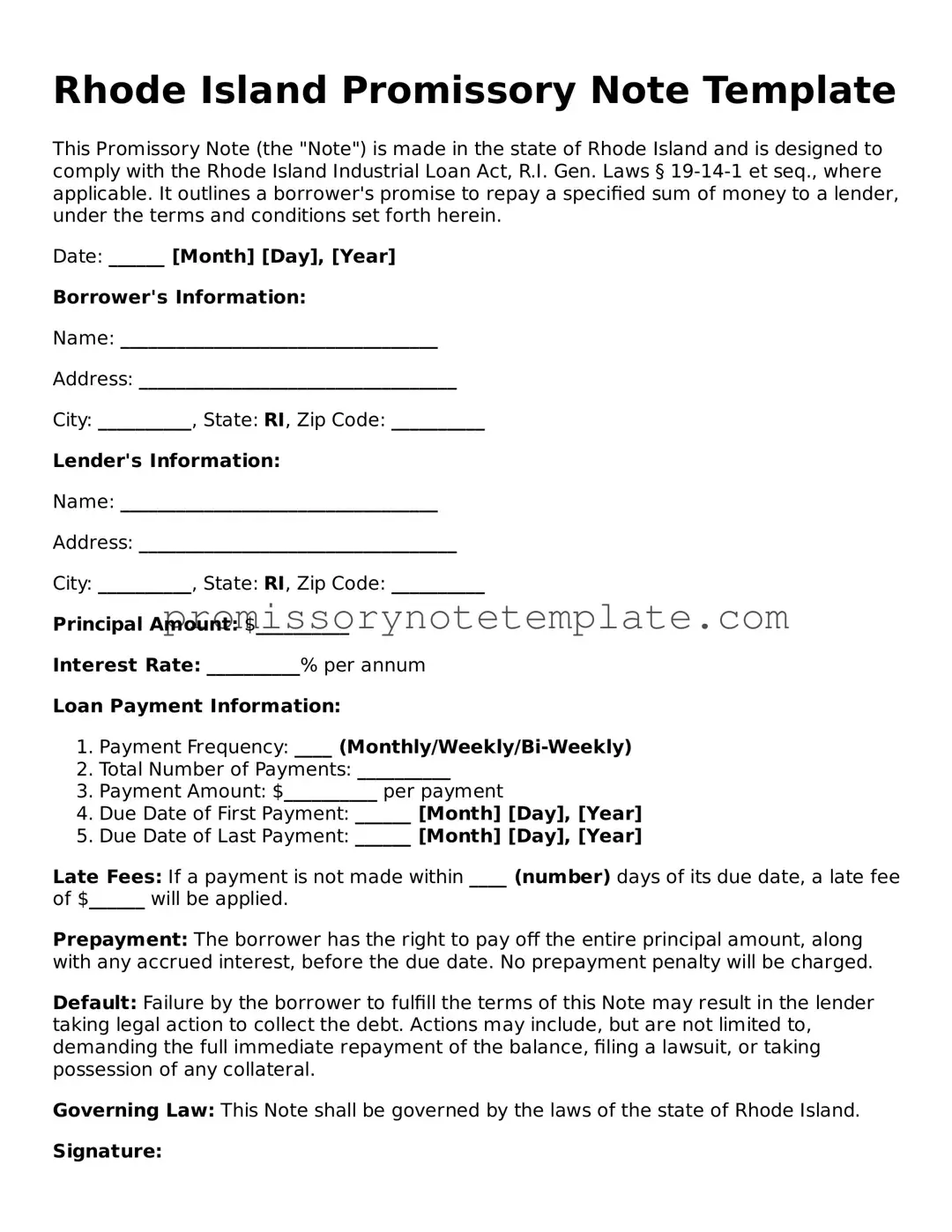

- Gather necessary information including the borrower's and lender's full legal names, addresses, and contact information.

- Decide on the loan amount and clearly write it both in numerical and written form to avoid any misunderstanding.

- Agree upon the interest rate for the loan. Remember, the rate must comply with Rhode Island's usury laws to prevent it from being considered illegal.

- Specify the loan's repayment schedule. Whether it’s in installments or a lump sum, clearly outline the dates and amounts for each payment.

- Detail any collateral securing the loan if the promissory note is secured. Describe the collateral in a manner that there’s no ambiguity regarding what is being pledged.

- Outline any late fees or penalties for missed payments within the terms. This ensures both parties are aware of the consequences of late or missed payments.

- Both parties should review the promissory note in full to ensure all the information is correct and understood fully.

- Include a section for signatures. Make sure both the borrower and the lender sign and date the promissory note. Witnesses or a notarization may also be required, depending on the complexity of the note.

Once the form is completed and signed, it becomes a legally binding document. Ensure both parties receive a copy for their records. Filling out the promissory note correctly is crucial for protecting the interests of both the lender and the borrower. Should disputes arise, the document serves as a crucial piece of evidence specifying the agreed-upon terms. Always consider consulting with a legal professional if there are uncertainties or complexities in your specific situation.