How to Use South Dakota Promissory Note

Filling out a promissory note in South Dakota can seem daunting at first, but it's a straightforward process designed to secure a financial agreement between two parties. It's a crucial step to ensure that both the borrower and the lender are protected and on the same page regarding the loan's terms and conditions. This guide is geared towards making sure that every step is clear, reducing confusion and bolstering confidence as you proceed. After following these steps, the form will be ready for use, setting the foundation for a respectful and legally binding financial relationship.

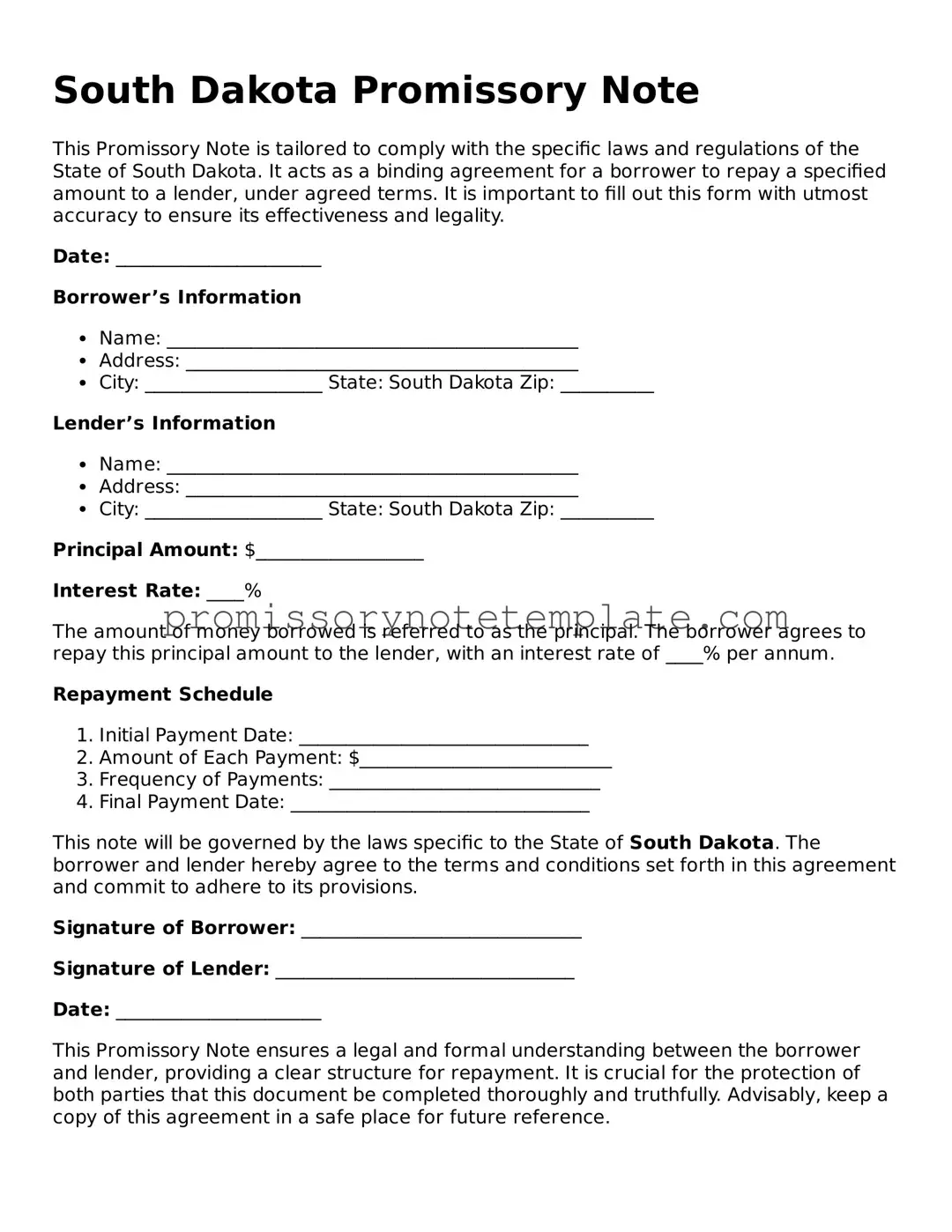

- Start by listing the full names and addresses of both the borrower and the lender at the top of the document. It's essential to use the legal names to avoid any confusion or legal issues in the future.

- Determine the loan amount and write it down in the designated space. Make sure this figure is accurate and agreed upon by both parties.

- Next, specify the interest rate annually. South Dakota has laws regulating the maximum interest rate; ensure the rate complies with state guidelines.

- Outline the repayment schedule. This includes when payments are due (e.g., monthly, quarterly), the number of payments, and when the first payment is due. Clarity here helps prevent misunderstandings later on.

- Decide on the method of payment. Whether it’s through bank transfers, checks, or another method, this should be agreed upon and noted.

- Include any collateral that the borrower is using to secure the loan. Clearly describe the collateral and state how it will be handled in case of default.

- Address late fees and penalties for missed payments. Providing these details helps reinforce the seriousness of the agreement and the expectations for timely repayment.

- If applicable, insert any co-signer information, including their full name and address. Co-signers provide an additional layer of security for the lender.

- Review the agreement with all parties involved. It’s important for everyone to understand and agree to the terms set forth in the document.

- Sign and date the promissory note. The document should be signed by the borrower, the lender, and any co-signers. These signatures officially activate the agreement.

- Finally, make copies of the signed promissory note. Each party should keep a copy for their records.

With the promissory note properly filled out, all parties will have a clear understanding of their obligations and rights regarding the loan. It forms the legal backbone of the financial agreement, helping to ensure that everyone involved is protected. As financial agreements can have lasting impacts, taking the time to carefully complete each step is crucial for a smooth and respectful borrowing and lending process.