How to Use Vermont Promissory Note

After deciding to create a Promissory Note in Vermont, understanding the steps to fill it out correctly is crucial. This legal document formalizes the promise to repay borrowed money under agreed terms and conditions, setting clear expectations between the borrower and lender. It's important to approach this task with attention to detail to ensure all the necessary information is correctly and clearly stated, adding a layer of security and understanding to the financial agreement. Following the proper steps to complete the form ensures that both parties are on the same page regarding the repayment plan, interest rate, and any other critical terms.

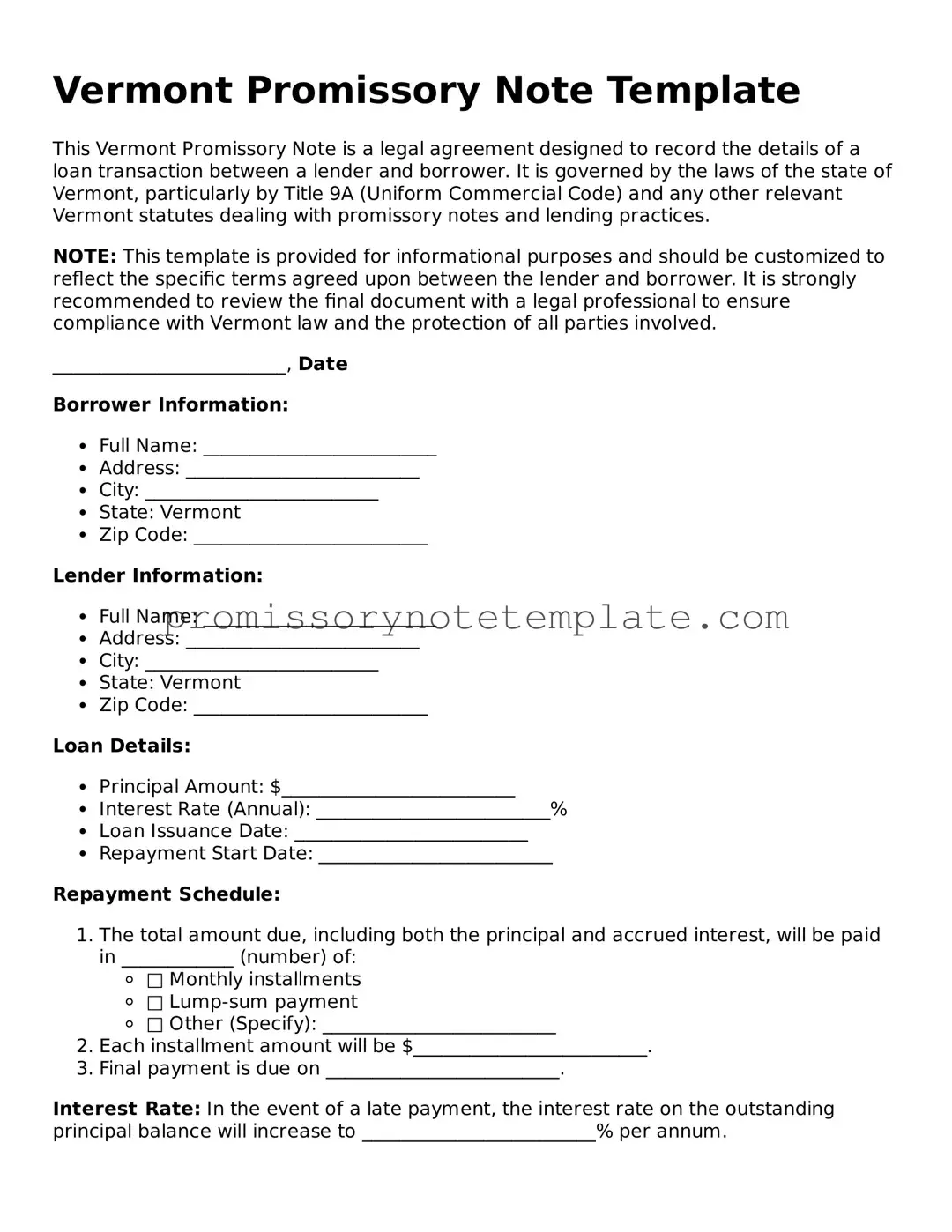

To successfully complete the Vermont Promissory Note form, please follow these steps:

- Enter the date the Promissory Note is being created at the top of the form.

- Write the full legal names and addresses of both the borrower and the lender in the designated sections.

- Specify the amount of money being loaned in both words and figures to avoid any confusion.

- Clearly state the interest rate annually. Make sure this rate complies with Vermont's usury laws to ensure the note's enforceability.

- Detail the repayment plan. Indicate whether it is in installments or a lump sum, the frequency of payments (monthly, quarterly, etc.), and the due date for the first payment and the final payment.

- If applicable, describe any collateral securing the loan. This adds assurance to the lender and details any property that can be claimed if the loan is not repaid.

- Include provisions for a co-signer if one is involved in the agreement. This person agrees to repay the loan if the original borrower fails to do so.

- Outline any actions that will be taken if the borrower fails to make payments. This may include late fees, acceleration of the repayment schedule, or legal action.

- Both the borrower and the lender must sign and date the Promissory Note. If applicable, have a co-signer sign the form too.

- Finally, it is recommended to have the signatures notarized to add an extra layer of authentication to the document.

With the form filled out accurately, both parties have created a legally binding document that outlines the details of the loan agreement. This clarity and formality help prevent misunderstandings and provide a clear path forward for both the repayment of the loan and the actions to be taken if the terms are not met. It's important for both the borrower and the lender to keep a copy of the signed Promissory Note for their records.