How to Use Virginia Promissory Note

When preparing to complete the Virginia Promissory Note form, individuals engage in a process aimed at creating a legal agreement related to borrowing and repaying a sum of money. This document serves to outline the terms and conditions of a loan between two parties, typically including details such as the amount borrowed, interest rate, repayment schedule, and any collateral involved. It is crucial that the information provided is accurate and reflects the agreement between the borrower and lender to ensure the enforceability of the document. The following steps are designed to guide individuals through the process of filling out the Virginia Promissory Note form efficiently.

- Start by entering the date the promissory note is being created at the top of the form.

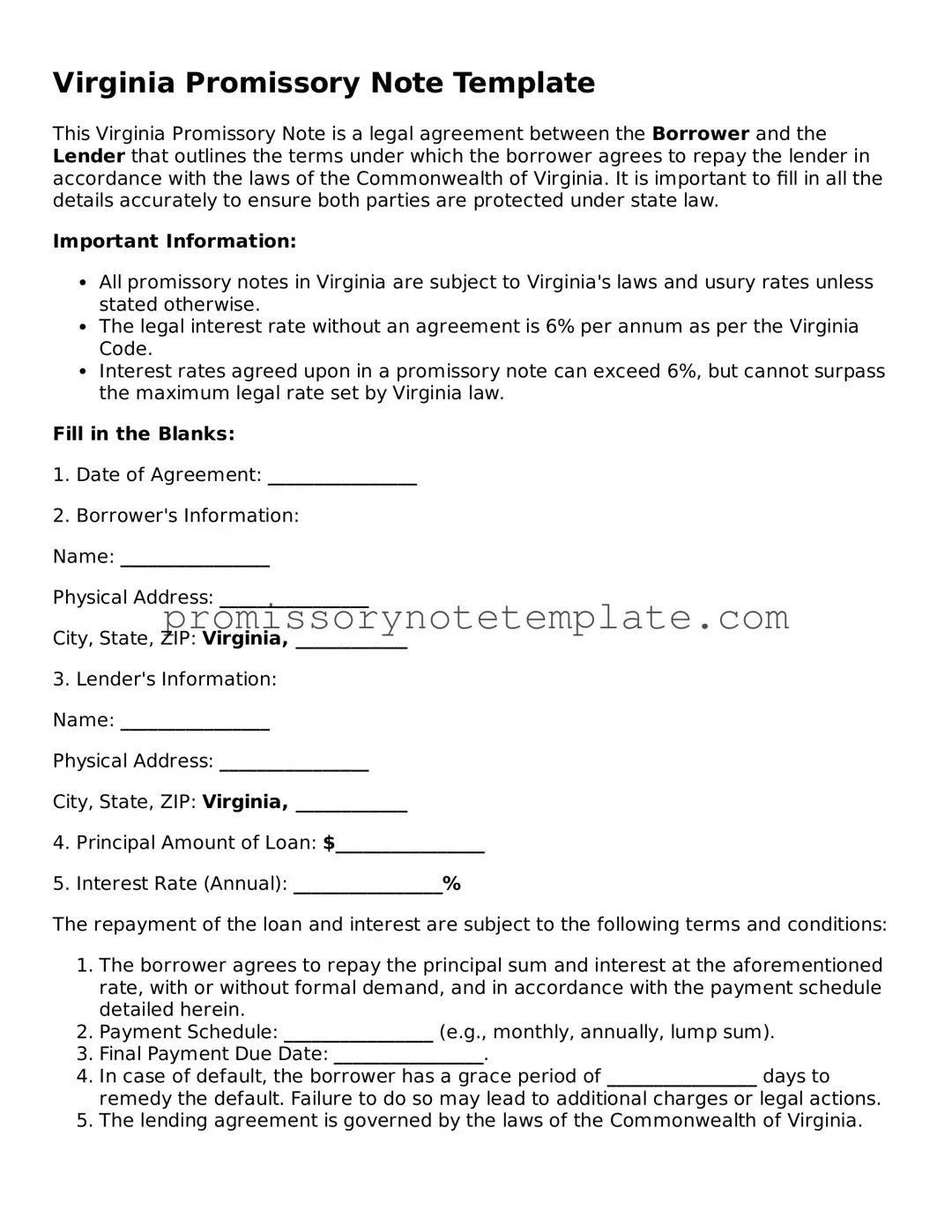

- Write the full name and address of the borrower in the space provided.

- Input the full name and address of the lender next to the borrower's information.

- Specify the total amount of money being borrowed, ensuring that it is written in both words and figures for clarity.

- Detail the interest rate per annum that will be applied to the principal amount. This must comply with Virginia state laws to avoid being considered usurious.

- Outline the repayment plan, including how often payments will be made (e.g., monthly), the amount of each payment, and when the first payment is due. Ensure all dates are complete and correct.

- If collateral is being used to secure the loan, describe the collateral in detail, including any identifying numbers or documentation, to ensure it is clear.

- Both parties should review the completed form to ensure all information is correct and reflects their agreement.

- Have the borrower sign and date the form. If a co-signer is part of the agreement, ensure they also sign and date the form.

- The lender should then sign and date the form, finalizing the agreement.

After completing these steps, it's essential to keep the Virginia Promissory Note in a safe place, as it serves as a legally binding document outlining the terms of the loan. Both parties may wish to make copies of the signed document for their records. Following the agreed-upon terms and maintaining open communication throughout the repayment period will help prevent any potential disputes.